�y�����o�ρz���������k�` ���̉\����441

1 �F���o�Â鏈�̖������F

��������o�ρA�R���A���ۏ�܂ŁA���{�̉ߋ��Ɩ�����^�ʖڂɂ���������X���ł��B

�݂�Ȓ��ǂ��A�r�炵�̓X���[�A�i�̂Ȃ��l�|�}�̓��[���ᔽ�B

�����̃X���́A�Ȃ�ׂ�sage�����ł��肢���܂��B�i���[�����ɔ��p�Ł@sage�@�����Ă��������j

�^�ʖڂȋ^�┽�_�劽�}�A�݂�ȂŒ��ǂ��l���܂��傤�B

>>950 ������k�`��~���Ď��X���𗧂Ă�ׂ��B

�O�X��

�y�����o�ρz���������k�` ���̉\����440

http://toki.2ch.net/test/read.cgi/asia/1318810945/

�ywktk�z�؍��o��ܸö�X�� 364won�y�ЂƂ��튦���~�����悤�āz

http://toki.2ch.net/test/read.cgi/asia/1319078949/

�ywktk�z�����o��ܸö�X�� 47���y�~�܂�Ȃ��`���C�i�{�J���z

http://toki.2ch.net/test/read.cgi/asia/1316516220/l50

�ywktk�z��p�o��ܸö�X�� 3NT$�y�q�Ɛl�ɕ����̌����̕������z

http://toki.2ch.net/test/read.cgi/asia/1263736028/

�ywktk�z���V�A�o��ܸö�X�� 15RUB

http://toki.2ch.net/test/read.cgi/asia/1300581025/

�y�������X�X�z�ɓ��œ牮 ���̃A�j���\ ��\�Z�t�ځy�������}�z

http://toki.2ch.net/test/read.cgi/asia/1313144301/

wktk�֘A���s�X���b�h�ꗗ(PC�p)

ttp://tokoyadangi.mokuren.ne.jp/html/wktkthreadlist.html

wktk�֘A���s�X���b�h�ꗗ(�g�їp)

ttp://tokoyadangi.mokuren.ne.jp/html/wktktl.html

�؍��o��wktk�X���܂Ƃ߃T�C�g Wiki ���̏����ߋ��X��

ttp://toanews.info/index.php?kako_tokoya

�݂�Ȓ��ǂ��A�r�炵�̓X���[�A�i�̂Ȃ��l�|�}�̓��[���ᔽ�B

�����̃X���́A�Ȃ�ׂ�sage�����ł��肢���܂��B�i���[�����ɔ��p�Ł@sage�@�����Ă��������j

�^�ʖڂȋ^�┽�_�劽�}�A�݂�ȂŒ��ǂ��l���܂��傤�B

>>950 ������k�`��~���Ď��X���𗧂Ă�ׂ��B

�O�X��

�y�����o�ρz���������k�` ���̉\����440

http://toki.2ch.net/test/read.cgi/asia/1318810945/

�ywktk�z�؍��o��ܸö�X�� 364won�y�ЂƂ��튦���~�����悤�āz

http://toki.2ch.net/test/read.cgi/asia/1319078949/

�ywktk�z�����o��ܸö�X�� 47���y�~�܂�Ȃ��`���C�i�{�J���z

http://toki.2ch.net/test/read.cgi/asia/1316516220/l50

�ywktk�z��p�o��ܸö�X�� 3NT$�y�q�Ɛl�ɕ����̌����̕������z

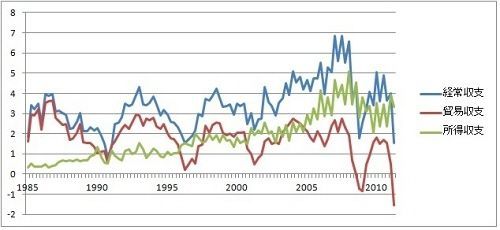

http://toki.2ch.net/test/read.cgi/asia/1263736028/

�ywktk�z���V�A�o��ܸö�X�� 15RUB

http://toki.2ch.net/test/read.cgi/asia/1300581025/

�y�������X�X�z�ɓ��œ牮 ���̃A�j���\ ��\�Z�t�ځy�������}�z

http://toki.2ch.net/test/read.cgi/asia/1313144301/

wktk�֘A���s�X���b�h�ꗗ(PC�p)

ttp://tokoyadangi.mokuren.ne.jp/html/wktkthreadlist.html

wktk�֘A���s�X���b�h�ꗗ(�g�їp)

ttp://tokoyadangi.mokuren.ne.jp/html/wktktl.html

�؍��o��wktk�X���܂Ƃ߃T�C�g Wiki ���̏����ߋ��X��

ttp://toanews.info/index.php?kako_tokoya

|

|

|

2 �F���o�Â鏈�̖������F2011/10/22(�y) 19:55:10.29 ID:cPtMHTW6

�e�����[�@�̊�b�m���B

ttp://blogs.yahoo.co.jp/daitojimari/folder/1639184.html

�ΐ��]�E���ɑ���\�ӏ�

1.�@ �^����������L�ۂ݂ɂ���ȁA�܂��͋^���B

2.�@ �����̓��ōl���Ă���C�ɂȂ�ȁA�w�ǂ̏ꍇ���ӎ��ɗU������Ă���Ǝv���B

3.�@ �������x�����ȁA�����ł����ӂ�����Α��삷�鎖�͉\���B

�@�@ ���v���Ă�͎Z�o���@����ő���ł����肷��B

4.�@ �ߋ��ɖڂ�������A�K�����ƌq�����Ă���B

5.�@ �F����l�ɓ������_�A�ӌ��ɒB�����Ƃ��́A���������͈����ȗU���A

�@�@ �ň����]����Ă���ƍl����B

6.�@ ���ہA���_�A���ʂ��ӏ������Ŕ����o���A�����Ċ֘A�t����B

7.�@ ���G��̗ǂ����t���茾���z�͐M�p����ȁB�����͉��S���B���Ă���B

8.�@ ���d�_���܂������Ă�z�͒P�Ȃ�p�t�H�[�}���X�ł���Ă邾�����B

�@�@ �o�b�N�ɋ���N���A�������͉�������ڂ���炷�ړI������ƍl����B

9.�@ ���_����q�ׂ�z�ɂ͋C������A�T�ⓚ�ɂȂ�B

10.�@����Ɗ������璼���ɓ�����B����Ɠ������̊m�ۂ�Y���ȁB

ttp://blogs.yahoo.co.jp/daitojimari/folder/1639184.html

�ΐ��]�E���ɑ���\�ӏ�

1.�@ �^����������L�ۂ݂ɂ���ȁA�܂��͋^���B

2.�@ �����̓��ōl���Ă���C�ɂȂ�ȁA�w�ǂ̏ꍇ���ӎ��ɗU������Ă���Ǝv���B

3.�@ �������x�����ȁA�����ł����ӂ�����Α��삷�鎖�͉\���B

�@�@ ���v���Ă�͎Z�o���@����ő���ł����肷��B

4.�@ �ߋ��ɖڂ�������A�K�����ƌq�����Ă���B

5.�@ �F����l�ɓ������_�A�ӌ��ɒB�����Ƃ��́A���������͈����ȗU���A

�@�@ �ň����]����Ă���ƍl����B

6.�@ ���ہA���_�A���ʂ��ӏ������Ŕ����o���A�����Ċ֘A�t����B

7.�@ ���G��̗ǂ����t���茾���z�͐M�p����ȁB�����͉��S���B���Ă���B

8.�@ ���d�_���܂������Ă�z�͒P�Ȃ�p�t�H�[�}���X�ł���Ă邾�����B

�@�@ �o�b�N�ɋ���N���A�������͉�������ڂ���炷�ړI������ƍl����B

9.�@ ���_����q�ׂ�z�ɂ͋C������A�T�ⓚ�ɂȂ�B

10.�@����Ɗ������璼���ɓ�����B����Ɠ������̊m�ۂ�Y���ȁB

3 �F���o�Â鏈�̖������F2011/10/22(�y) 19:55:28.20 ID:cPtMHTW6

�A�}�`���A�����̓����댯��m��Ȃ����C�ߏ��]������B

�A�}�`���A�̘_��

�E���z�_���K�͘_�ɂ���

�E�����҂̔\�͂�w�͂�m�炸�C���\�E���ӔC�E�ӑĂƔᔻ����B

�E�v���́C�~�X�������C�܂��C�ω���댯��\�m�ł��鑶�݂ƌ��߂��C

�@����ɔ����鎖�̂���������v�����i�Ɣᔻ���C���ɂ́C�ƍߎ҂ɂ���B

�E������ƁC�댯�Ȃ��Ƃ��ȒP�ɍl���C�u���v�ƌ������u�f�l�̖\�_�v

�E�����⎸�s�̗��R���C�P�`�Q�̗v�f�ɋ��߁C�Z���I�ɗ������C�_����B

�@���Ɂu�A�C�f�A�v�C�u�ӎ��v�C�u�̎��v�C�u���x�v�C�u�g�D�\���v�Ȃǂɋ��߂�B

��

�E���݂̐��x�̃f�����b�g�݂̂������炤�B

�E�V���Ȑ��x�̃����b�g�݂̂��A�s�[�����Ē���B

�E�V���Ȑ��x�̃f�����b�g�C����p���l���Ȃ��i�m��Ȃ��H�j�B

��

�E�V���Ȑ��x����������C�ɉ�������ƍl���C���v��v����A�Ă���B

�E�ł��Ȃ����R���C���v����z���͂�ӗ~�̕s���ɋ��߂�B

�E�g���[�h�I�t������ۑ���C�����ɂ��Ƃ����i���Ƃ��C�v���ƓI�m�j�B

�A�}�`���A�̘_��

�E���z�_���K�͘_�ɂ���

�E�����҂̔\�͂�w�͂�m�炸�C���\�E���ӔC�E�ӑĂƔᔻ����B

�E�v���́C�~�X�������C�܂��C�ω���댯��\�m�ł��鑶�݂ƌ��߂��C

�@����ɔ����鎖�̂���������v�����i�Ɣᔻ���C���ɂ́C�ƍߎ҂ɂ���B

�E������ƁC�댯�Ȃ��Ƃ��ȒP�ɍl���C�u���v�ƌ������u�f�l�̖\�_�v

�E�����⎸�s�̗��R���C�P�`�Q�̗v�f�ɋ��߁C�Z���I�ɗ������C�_����B

�@���Ɂu�A�C�f�A�v�C�u�ӎ��v�C�u�̎��v�C�u���x�v�C�u�g�D�\���v�Ȃǂɋ��߂�B

��

�E���݂̐��x�̃f�����b�g�݂̂������炤�B

�E�V���Ȑ��x�̃����b�g�݂̂��A�s�[�����Ē���B

�E�V���Ȑ��x�̃f�����b�g�C����p���l���Ȃ��i�m��Ȃ��H�j�B

��

�E�V���Ȑ��x����������C�ɉ�������ƍl���C���v��v����A�Ă���B

�E�ł��Ȃ����R���C���v����z���͂�ӗ~�̕s���ɋ��߂�B

�E�g���[�h�I�t������ۑ���C�����ɂ��Ƃ����i���Ƃ��C�v���ƓI�m�j�B

4 �F���o�Â鏈�̖������F2011/10/22(�y) 19:55:45.62 ID:cPtMHTW6

���̌��t��S�ɒ@������

��A�@�אڂ��鍑�݂͌��ɓG����B

��A�@�G�̓G�͐�p�I�Ȗ����ł���B

�O�A�@�G���Ă��Ă��A���a�ȊW����邱�Ƃ͂ł���B

�l�A�@���ۊW�́A�P���łȂ������ōl����B

�܁A�@���ۊW�͗��p�ł��邩�A���p����Ă��Ȃ����ōl����B

�Z�A�@�D�ꂽ���R�卑�������ɊC�R�卑�����˂邱�Ƃ͂ł��Ȃ��i���̋t���R��j

���A�@���ې������Ō���B�P�����������܂Ȃ��B

���A�@�O���𗘗p�ł��邩�l����B

��A�@���{�����p����Ă���̂ł͂Ȃ����^���B

�\�A�@�ړI�͎����̐����Ɣ��W����

�\��A��i�͑I�Ȃ�

�\��A�����������l����B���`�͋[���ł���B

�\�O�A���ۊW���Q���Ԃ����łȂ��C�����ԓI�ɍl����B

�\�l�A���f���Ȃ�

�\�܁A�F�D�C������^�ɎȂ�

�\�Z�A�O��I�ɐl�������l���ɗ���

�\���A�Ȋw�Z�p�̔��B���l������

�u���Ƃɐ^�̗F�l�͂��Ȃ��v�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�@�L�b�V���W���[

�u�����������鍑�͖łт�v�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�@�}�L���׃�

�u�䂪���ȊO�͑S�ĉ��z�G���ł���v�c�c�c�c�c�c�c�c�c�c�c�c�c�@�`���[�`��

�u�����Ɠ����҂́A���̉ߒ��Ŏ��炪�����Ɖ����ʂ悤�S����B

�@�����[����`���҂��A�[�����܂����������Ԃ��v�c�c�c�c�c�c�c�c�c�@�t���[�h���q�E�j�[�`�F

�u�ߎ�����Ĕ�����ꂸ�A���тȂ��܂���A�����łт�v�c�c�c�@�ؔ�q

�u���a��]�ނȂ�A�푈�ɔ�����B�iSi vis pacem, para bellum.�j�v�c�c�@���e����̊i��

�u�ߊώ�`�͋C���ɂ����̂ł���A

�@�@�@�@�@�@�@�@�@�@�@�@�@�y�ώ�`�͈ӎu�ɂ����̂ł���B�v�@�@�@�c�c�@�A����

��A�@�אڂ��鍑�݂͌��ɓG����B

��A�@�G�̓G�͐�p�I�Ȗ����ł���B

�O�A�@�G���Ă��Ă��A���a�ȊW����邱�Ƃ͂ł���B

�l�A�@���ۊW�́A�P���łȂ������ōl����B

�܁A�@���ۊW�͗��p�ł��邩�A���p����Ă��Ȃ����ōl����B

�Z�A�@�D�ꂽ���R�卑�������ɊC�R�卑�����˂邱�Ƃ͂ł��Ȃ��i���̋t���R��j

���A�@���ې������Ō���B�P�����������܂Ȃ��B

���A�@�O���𗘗p�ł��邩�l����B

��A�@���{�����p����Ă���̂ł͂Ȃ����^���B

�\�A�@�ړI�͎����̐����Ɣ��W����

�\��A��i�͑I�Ȃ�

�\��A�����������l����B���`�͋[���ł���B

�\�O�A���ۊW���Q���Ԃ����łȂ��C�����ԓI�ɍl����B

�\�l�A���f���Ȃ�

�\�܁A�F�D�C������^�ɎȂ�

�\�Z�A�O��I�ɐl�������l���ɗ���

�\���A�Ȋw�Z�p�̔��B���l������

�u���Ƃɐ^�̗F�l�͂��Ȃ��v�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�@�L�b�V���W���[

�u�����������鍑�͖łт�v�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�c�@�}�L���׃�

�u�䂪���ȊO�͑S�ĉ��z�G���ł���v�c�c�c�c�c�c�c�c�c�c�c�c�c�@�`���[�`��

�u�����Ɠ����҂́A���̉ߒ��Ŏ��炪�����Ɖ����ʂ悤�S����B

�@�����[����`���҂��A�[�����܂����������Ԃ��v�c�c�c�c�c�c�c�c�c�@�t���[�h���q�E�j�[�`�F

�u�ߎ�����Ĕ�����ꂸ�A���тȂ��܂���A�����łт�v�c�c�c�@�ؔ�q

�u���a��]�ނȂ�A�푈�ɔ�����B�iSi vis pacem, para bellum.�j�v�c�c�@���e����̊i��

�u�ߊώ�`�͋C���ɂ����̂ł���A

�@�@�@�@�@�@�@�@�@�@�@�@�@�y�ώ�`�͈ӎu�ɂ����̂ł���B�v�@�@�@�c�c�@�A����

5 �F���o�Â鏈�̖������F2011/10/22(�y) 19:56:02.09 ID:cPtMHTW6

������`�̂��߂�7�̖@��

�@1�u�l�[���E�R�[�����O�v

�@�@�@�U���Ώۂ̐l���E�W�c�E�g�D�Ȃǂɑ��A�����⋰�|�̊���ɑi����}�C�i�X�̃��b�e����\��i���x�����O�j�B

�@�@�@���f�B�A��l�b�g�ɂ���ČJ��Ԃ��������X�e���I�^�C�v�̏��ɂ��A����M�҂́A���X�ɑΏۂɑ�����

�@�@�@�[�߂Ă����B

�@2�u�ؗ�Ȍ��t�ɂ�镁�Չ��v

�@�@�@���肽�Ă����t�Ŏ��������̍s�ׂ𐳓������Ă��܂��B

�@�@�@����̂��悤�̂Ȃ��E�����炢�t���[�Y�E���`���������A��������藧�Ă�B

�@3�u�]���v

�@�@�@���܂��܂Ȍ��Ђ�Ќ���p���āA���������̈ӌ���ړI����@�𐳓�������A����������������B

�@4�u�،����p�v

�@�@�@���h�����E���Ђ���l�����g���āA���������̈ӌ���ړI����@�����������Ƃ��،��E�㉇������B

�@5�u���}���v

�@�@�@���������̏�������A����M�҂Ɠ�������E�����ł��邱�Ƃ��������A���S�⋤����e�ߊ��A��̊��������o���B

�@6�u�J�[�h�X�^�b�L���O�v

�@�@�@�s���̂����������������A�s���������������⏬��������B�������肷��B

�@7�u�o���h���S���v

�@�@�@�傫�Ȋy�����ڂ��䂭�悤�ɁA���̎������A���̒��̐����ł��邩�̂悤�ɐ�`����B

�@�@�@����M�҂́A����ɏ]��Ȃ����Ƃɂ����c������I�s�����o���A

�@�@�@���ǂ͂��́u�y���v�ɓ������Ă������ƂɂȂ�B

�@1�u�l�[���E�R�[�����O�v

�@�@�@�U���Ώۂ̐l���E�W�c�E�g�D�Ȃǂɑ��A�����⋰�|�̊���ɑi����}�C�i�X�̃��b�e����\��i���x�����O�j�B

�@�@�@���f�B�A��l�b�g�ɂ���ČJ��Ԃ��������X�e���I�^�C�v�̏��ɂ��A����M�҂́A���X�ɑΏۂɑ�����

�@�@�@�[�߂Ă����B

�@2�u�ؗ�Ȍ��t�ɂ�镁�Չ��v

�@�@�@���肽�Ă����t�Ŏ��������̍s�ׂ𐳓������Ă��܂��B

�@�@�@����̂��悤�̂Ȃ��E�����炢�t���[�Y�E���`���������A��������藧�Ă�B

�@3�u�]���v

�@�@�@���܂��܂Ȍ��Ђ�Ќ���p���āA���������̈ӌ���ړI����@�𐳓�������A����������������B

�@4�u�،����p�v

�@�@�@���h�����E���Ђ���l�����g���āA���������̈ӌ���ړI����@�����������Ƃ��،��E�㉇������B

�@5�u���}���v

�@�@�@���������̏�������A����M�҂Ɠ�������E�����ł��邱�Ƃ��������A���S�⋤����e�ߊ��A��̊��������o���B

�@6�u�J�[�h�X�^�b�L���O�v

�@�@�@�s���̂����������������A�s���������������⏬��������B�������肷��B

�@7�u�o���h���S���v

�@�@�@�傫�Ȋy�����ڂ��䂭�悤�ɁA���̎������A���̒��̐����ł��邩�̂悤�ɐ�`����B

�@�@�@����M�҂́A����ɏ]��Ȃ����Ƃɂ����c������I�s�����o���A

�@�@�@���ǂ͂��́u�y���v�ɓ������Ă������ƂɂȂ�B

6 �F���o�Â鏈�̖������F2011/10/22(�y) 19:56:16.91 ID:cPtMHTW6

�F�l���ȉ��́u�k�ق̓����P�T���v���o���A���������y��r�����܂��傤�B

�P�F�����ɑ��ĉ���������o��

�Q�F�����܂�Ȕ�����Ƃ肠����

�R�F�����ɗL���ȏ�������\�z����

�S�F��ςŌ��ߕt����

�T�F���������������_���x������Ă���Ǝv�킹��

�U�F�ꌩ�W���肻���ŊW�Ȃ��b���n�߂�

�V�F�A�d�ł���Ɨ͐�����

�W�F�m�\��Q���N����

�X�F�����̌������q�ׂ��ɐl�i�ᔻ������

10�F���肦�Ȃ��������}��

11�F���b�e���\�������

12�F���������b���o�܂����ď����Ԃ�

13�F�����錾������

14�F�ׂ��������̃~�X���w�E������m�ƔF��������

15�F�V�����T�O���S�Đ������̂��ƃ~�X���[�h����

�P�F�����ɑ��ĉ���������o��

�Q�F�����܂�Ȕ�����Ƃ肠����

�R�F�����ɗL���ȏ�������\�z����

�S�F��ςŌ��ߕt����

�T�F���������������_���x������Ă���Ǝv�킹��

�U�F�ꌩ�W���肻���ŊW�Ȃ��b���n�߂�

�V�F�A�d�ł���Ɨ͐�����

�W�F�m�\��Q���N����

�X�F�����̌������q�ׂ��ɐl�i�ᔻ������

10�F���肦�Ȃ��������}��

11�F���b�e���\�������

12�F���������b���o�܂����ď����Ԃ�

13�F�����錾������

14�F�ׂ��������̃~�X���w�E������m�ƔF��������

15�F�V�����T�O���S�Đ������̂��ƃ~�X���[�h����

7 �F���o�Â鏈�̖������F2011/10/22(�y) 19:56:25.63 ID:cPtMHTW6

�@|| ���r�炵�͕��u����ԃL���C�B�r�炵�͏�ɒN���̔�����҂��Ă��܂��B

�@|| ���d���X���ɂ͗U�������N��\���ĕ��u�B�E�U�C�Ǝv�����炻�̂܂ܕ��u�B

�@|| �����u���ꂽ�r�炵�͐���⎩�쎩���ł��Ȃ��̃��X��U���܂��B

�@||�@�@�m�Z���ă��X�����炻�̎��_�ł��Ȃ��̕����B

�@|| �������͍r�炵�̎��{�ɂ��ĉh�{�ł���ł���Ԃ��Ƃł��B�r�炵�ɃG�T��

�@||�@�@�^���Ȃ��ʼn������B�@�@�@�@�@�@�@�@�@�@�@�@�@�@�@�@ ��_��

�@|| ���͎�����܂ŌǓƂɖ\�ꂳ���Ă����ā@�@ �_�@(߁[�*)�@��݁B

�@||�@�@�S�~�����܂�����폜����Ԃł��B�@�@�@�@�@ �@���� |

�@||�Q�Q�Q �� �ȁQ�Q�� �ȁQ�Q�@�� �ȁQ�@�@�@�@�@ |�P�P�P�P|

�@�@�@�@�@�@(�@ �� ��__ (�@�@ �� ��__(�@�@ �� �ȁ@�@�@�@�P�P�P�P�P

�@�@�@�@�`�i�Q(�@�@�� �ȁQ (�@ �� �ȁQ (�@�@�� �� �@�́`���A�搶�B

�@�@�@�@�@�@�`�i�Q(�@ �@,,)�`�i�Q(�@ �@,,)�`�i�Q(�@ �@,,)

�@�@�@�@�@�@�@�@�`�i�Q__Ɂ@�@�`�i�Q__� �@�@�`�i�Q__�

8 �F���o�Â鏈�̖������F2011/10/22(�y) 20:08:29.05 ID:Zx1ak2Hl

ttp://www.yomiuri.co.jp/atmoney/news/20111022-OYT1T00677.htm

�M���V����@�A���ɔ�щΌ��O�c�ɑO���x���@�i2011�N10��22��19��52�� �ǔ��V���j

���[�����n�݂ɍv�������C�^���A�̃��}�[�m�E�v���[�f�B�O�i�V�Q�j�͂Q�O���A�{���̃C���^�r���[�ŁA�Q�R���̉��B�A���i�d�t�j��]��c

��O�Ɂu�t�����X���i���́j�i�����̋���ɒ��ʂ��Ă���v�Ǝw�E���A�d�t�����B�����E���Z��@�̎������ł��o���Ȃ���A�u�t�����X��

�̑Ō����傫���Ȃ�v�ƌx�������B

�M���V����@�ɔ����M�p�s�����C�^���A�A�X�y�C���̂ق��A�t�����X�ɂ���щ��鎖�Ԃɋ������O�����������̂��B�v���[�f�B���́A���[����

�ً̋}�x�����x�u���B���Z�������i�d�e�r�e�j�v�̗Z���\�͋�������@�g��h�~�ɗL���Ƃ̍l�������������B

��A�̊�@�̌����ɂ��ẮA�d�t���ǂ̊Ď��\�͕s�����M���V���̍��B�����������Ƃ̌�����A�ʉ݊Ǘ���o�ρE��������ł̂d�t�̌����s

�����w�E���A���[�����̍\�����u�������v�ƒf�����B�d�t�̈ӎv����Ɋւ��Ă��u�S���v�͉��B�̓G���v�Ƃ��A�������̐l����Ŋe���ɕ[����

�蓖�Ă�u���葽�����v�����p���Đv��������悤���߂��B

-------------------------------------------------------------------------------------------------------------------------------

���d�t���ǂ̊Ď��\�͕s�����M���V���̍��B����������

����ɂ�A�����I�v���p�K���_�Ƃ��Ẳ��B����̃V���{���Ƃ��Ė������M���V����EU�Ɏ����������h�̐����Ƃ����̂��Ԕ��v�l���iry

�M���V����@�A���ɔ�щΌ��O�c�ɑO���x���@�i2011�N10��22��19��52�� �ǔ��V���j

���[�����n�݂ɍv�������C�^���A�̃��}�[�m�E�v���[�f�B�O�i�V�Q�j�͂Q�O���A�{���̃C���^�r���[�ŁA�Q�R���̉��B�A���i�d�t�j��]��c

��O�Ɂu�t�����X���i���́j�i�����̋���ɒ��ʂ��Ă���v�Ǝw�E���A�d�t�����B�����E���Z��@�̎������ł��o���Ȃ���A�u�t�����X��

�̑Ō����傫���Ȃ�v�ƌx�������B

�M���V����@�ɔ����M�p�s�����C�^���A�A�X�y�C���̂ق��A�t�����X�ɂ���щ��鎖�Ԃɋ������O�����������̂��B�v���[�f�B���́A���[����

�ً̋}�x�����x�u���B���Z�������i�d�e�r�e�j�v�̗Z���\�͋�������@�g��h�~�ɗL���Ƃ̍l�������������B

��A�̊�@�̌����ɂ��ẮA�d�t���ǂ̊Ď��\�͕s�����M���V���̍��B�����������Ƃ̌�����A�ʉ݊Ǘ���o�ρE��������ł̂d�t�̌����s

�����w�E���A���[�����̍\�����u�������v�ƒf�����B�d�t�̈ӎv����Ɋւ��Ă��u�S���v�͉��B�̓G���v�Ƃ��A�������̐l����Ŋe���ɕ[����

�蓖�Ă�u���葽�����v�����p���Đv��������悤���߂��B

-------------------------------------------------------------------------------------------------------------------------------

���d�t���ǂ̊Ď��\�͕s�����M���V���̍��B����������

����ɂ�A�����I�v���p�K���_�Ƃ��Ẳ��B����̃V���{���Ƃ��Ė������M���V����EU�Ɏ����������h�̐����Ƃ����̂��Ԕ��v�l���iry

9 �F���o�Â鏈�̖������F2011/10/22(�y) 20:16:54.94 ID:QqV3H5rt

�M���V���͗\�z�ȏ�Ɉ����݂����ł��ȁE�E�E

10 �F���o�Â鏈�̖������F2011/10/22(�y) 20:29:29.88 ID:NUaqwjFA

��������

>>8

���u�S���v�͉��B�̓G���v�Ƃ��A�������̐l����Ŋe���ɕ[����

���蓖�Ă�u���葽�����v�����p���Đv��������悤���߂��B

�l���E�E�E�E�E���Ă̂͂ǂ����낤�Ȃ��H�����n�̔����͂��k���ɔ�ׂ�

�����Ȃ肷�����Ȃ����H

�܂��C�^���A���t�����X�ɐl���ł��Č����̂͂悭�킩�邯�ǁB

>>8

���u�S���v�͉��B�̓G���v�Ƃ��A�������̐l����Ŋe���ɕ[����

���蓖�Ă�u���葽�����v�����p���Đv��������悤���߂��B

�l���E�E�E�E�E���Ă̂͂ǂ����낤�Ȃ��H�����n�̔����͂��k���ɔ�ׂ�

�����Ȃ肷�����Ȃ����H

�܂��C�^���A���t�����X�ɐl���ł��Č����̂͂悭�킩�邯�ǁB

11 �F���o�Â鏈�̖������F2011/10/22(�y) 20:31:19.88 ID:cPtMHTW6

�������o�ϐ�D���`�ȃg���R�����Ă����Ηǂ������̂ɂ˂��c��EU

12 �F���o�Â鏈�̖������F2011/10/22(�y) 20:56:20.64 ID:NUaqwjFA

�o�ϗ͂Ȃ炽�Ԃ�܂��܂����낤�B

�����͂���������IMF�݂����Ȋ��呍������ɂ���Έ�Ԏ��p�I���Ǝv�����ǁA

���Ԃ��炶�イ�Ńu�`�M����l�������o�邩�疳�����낤�ȁB

�����͂���������IMF�݂����Ȋ��呍������ɂ���Έ�Ԏ��p�I���Ǝv�����ǁA

���Ԃ��炶�イ�Ńu�`�M����l�������o�邩�疳�����낤�ȁB

13 �F���o�Â鏈�̖������F2011/10/22(�y) 21:18:41.49 ID:Zx1ak2Hl

ttp://www.nikkei.com/news/headline/article/g=96958A9C9381959FE0E0E2E19F8DE0E0E3E2E0E2E3E3E2E2E2E2E2E2

�o���R�N�s�S�����Z���@�h���炪���� �@2011/10/22 20:41

�@

�y�o���R�N���ɓ��w�z�^����Q�������^�C�̎�s�o���R�N��22���A��s���S���𗬂��`���I�v������̈ꕔ�Ŗh���炪���A���ӓ��H��

�Z�����n�܂����B����̍^���ŁA�^�C���{�̓o���R�N�s�S�����Z�����Ȃ��悤������̖h�q����~���Ă������A���߂Đ������ꍞ�B���n

���f�B�A�ɂ��A�Z���͍ő�40�Z���`���Ƃ����B

�ɂ��A�`���I�v�����삪�×������͎̂�s�̓s�S���ɂ���T���Z���ʂ�B�ʂ�߂��ɂ̓^�C������s������ق��A��ɐ��L���̋���

�Ƀ^�C���{���ʒu����B�Z���̏ڂ��������͖��炩�ɂȂ��Ă��Ȃ����A�k�����牟�����^���ɂ���̐��ʂ��㏸�B�h���炪���A��

�����ӂ�o�����̂Ƃ݂���B

�s�S���ɂ͓��{�l�w�Z����{�l���݈����Z�ދ��Z�n�悪����B�݃^�C���{��g�ق͍���̔×����܂߂āA23���Ƀ^�C�ݗ��M�l������������J

�����Ƃ����߂��B

�o���R�N�s�S�����Z���@�h���炪���� �@2011/10/22 20:41

�@

�y�o���R�N���ɓ��w�z�^����Q�������^�C�̎�s�o���R�N��22���A��s���S���𗬂��`���I�v������̈ꕔ�Ŗh���炪���A���ӓ��H��

�Z�����n�܂����B����̍^���ŁA�^�C���{�̓o���R�N�s�S�����Z�����Ȃ��悤������̖h�q����~���Ă������A���߂Đ������ꍞ�B���n

���f�B�A�ɂ��A�Z���͍ő�40�Z���`���Ƃ����B

�ɂ��A�`���I�v�����삪�×������͎̂�s�̓s�S���ɂ���T���Z���ʂ�B�ʂ�߂��ɂ̓^�C������s������ق��A��ɐ��L���̋���

�Ƀ^�C���{���ʒu����B�Z���̏ڂ��������͖��炩�ɂȂ��Ă��Ȃ����A�k�����牟�����^���ɂ���̐��ʂ��㏸�B�h���炪���A��

�����ӂ�o�����̂Ƃ݂���B

�s�S���ɂ͓��{�l�w�Z����{�l���݈����Z�ދ��Z�n�悪����B�݃^�C���{��g�ق͍���̔×����܂߂āA23���Ƀ^�C�ݗ��M�l������������J

�����Ƃ����߂��B

14 �F���o�Â鏈�̖������F2011/10/22(�y) 21:24:40.41 ID:oxpEARiS

15 �F���o�Â鏈�̖������F2011/10/22(�y) 21:45:53.66 ID:GKsAmW+A

>>8

�C�^���A�Ɍ�����Ȃ�ā[

�C�^���A�Ɍ�����Ȃ�ā[

16 �F���o�Â鏈�̖������F2011/10/22(�y) 21:55:01.08 ID:GJDeKaty

>>15

���I������������̂ɁA�����ɒm�点�Ă��瓊������Ȃ�ăA�z�̂��邱�Ƃ��B

���I�����������Ă��玖�����悩�����̂ɁB

�����`�̎�_�Ƃ���ƁA�����͌��I�������K�c���Ɠ������B

���I������������̂ɁA�����ɒm�点�Ă��瓊������Ȃ�ăA�z�̂��邱�Ƃ��B

���I�����������Ă��玖�����悩�����̂ɁB

�����`�̎�_�Ƃ���ƁA�����͌��I�������K�c���Ɠ������B

17 �F���o�Â鏈�̖������F2011/10/22(�y) 22:03:06.03 ID:Zx1ak2Hl

���a�}�̑哝�̌��̈�l�ō��l��Herman Cain��CNN�̃C���^�r���[�̒��Œ�����ɂ��āu�v���E�`���C�X�v�h�Ǝ��ꂩ�˂Ȃ�

���������Đ����I�g��B�ꕔ�ɂ͂��̔������v���I�Ƃ����������B

-------------------------------------------------------------------------------------------------------------------------

ttp://www.tnr.com/article/the-permanent-campaign/96544/cain-abortion-iowa-gop-2012-tax-plan

Why There�fs No Way Cain Will Survive His Abortion Gaffe Ed Kilgore October 22, 2011 | 12:00 am

Cain�fs improbable rise in national and early-state polls would now end, they probably figured, as GOP voters discovered the pizza

man�fs signature policy proposal wasn�ft terribly well thought out. But it�fs likely that Cain could have overcome the criticisms

surrounding his tax proposal. What he will struggle to live down, on the other hand, are his recent comments on abortion.

���������Đ����I�g��B�ꕔ�ɂ͂��̔������v���I�Ƃ����������B

-------------------------------------------------------------------------------------------------------------------------

ttp://www.tnr.com/article/the-permanent-campaign/96544/cain-abortion-iowa-gop-2012-tax-plan

Why There�fs No Way Cain Will Survive His Abortion Gaffe Ed Kilgore October 22, 2011 | 12:00 am

Cain�fs improbable rise in national and early-state polls would now end, they probably figured, as GOP voters discovered the pizza

man�fs signature policy proposal wasn�ft terribly well thought out. But it�fs likely that Cain could have overcome the criticisms

surrounding his tax proposal. What he will struggle to live down, on the other hand, are his recent comments on abortion.

18 �F���o�Â鏈�̖������F2011/10/22(�y) 22:04:53.90 ID:rPe2U+Yr

����ǂ������b�H

��Ǝ抪��������ł��Ȃ��w�C���Ă����Ď��H

�I�����p�X�O�В��E�b�h�t�H�[�h���u����͑g�D�I�Ȕƍ߂��B�e�썄��͉�Ђ⍑���Ă���v

http://hatsukari.2ch.net/test/read.cgi/news/1319282062/

��Ǝ抪��������ł��Ȃ��w�C���Ă����Ď��H

�I�����p�X�O�В��E�b�h�t�H�[�h���u����͑g�D�I�Ȕƍ߂��B�e�썄��͉�Ђ⍑���Ă���v

http://hatsukari.2ch.net/test/read.cgi/news/1319282062/

19 �F���o�Â鏈�̖������F2011/10/22(�y) 22:07:37.79 ID:Zx1ak2Hl

>>17 ���x��������݂�ƁA���a�}�哝�̌�₪Herman Cain�ɂȂ�Ƃ����͈̂����̂悤�ȃV�i���I�ŁA�I�o�}�̍ŋ��x�����͂̍��l�w��

�}�C�m���e�B�ւ̖���}�̐����͂������Ȃ�B���̔����ň�Ԋ��ł���̂̓��x�����̂悤�ŁE�E�E

�}�C�m���e�B�ւ̖���}�̐����͂������Ȃ�B���̔����ň�Ԋ��ł���̂̓��x�����̂悤�ŁE�E�E

20 �F���o�Â鏈�̖������F2011/10/22(�y) 22:15:17.61 ID:NUaqwjFA

>>18

����̘b�Ɋւ��Ă̓I�����p�X�������̐����͂܂������Ӗ����Ȃ��ĂȂ��B

�悭�����Ƃ���ɐH�����ꂽ��Ȃ����Ƃ��������B�܂��K�͂͌��ňႤ���ǁB

�����A�E�b�h�t�H�[�h�������������Ƃ����Ƃ������͂悭�킩��Ȃ��B

����̘b�Ɋւ��Ă̓I�����p�X�������̐����͂܂������Ӗ����Ȃ��ĂȂ��B

�悭�����Ƃ���ɐH�����ꂽ��Ȃ����Ƃ��������B�܂��K�͂͌��ňႤ���ǁB

�����A�E�b�h�t�H�[�h�������������Ƃ����Ƃ������͂悭�킩��Ȃ��B

21 �F���o�Â鏈�̖������F2011/10/22(�y) 22:17:13.34 ID:GJDeKaty

>>18

http://news.yahoo.com/exclusive-olympus-trail-reaches-elusive-bankers-florida-home-011044828.html

http://news.yahoo.com/exclusive-olympus-trail-reaches-elusive-bankers-florida-home-011044828.html

22 �F���o�Â鏈�̖������F2011/10/22(�y) 22:28:01.03 ID:Q7yTIwvh

�r�c�����đn���������̂���c ���h���Ă��̂Ɂc�V���b�N���c

23 �F���o�Â鏈�̖������F2011/10/22(�y) 22:29:13.84 ID:yC9VZHPc

���̃W���[�N����A��������ň�ԏ���> 22

24 �F���o�Â鏈�̖������F2011/10/22(�y) 22:31:04.67 ID:NUaqwjFA

��̓I�ɃI�����p�X���\��������ttp://www.olympus.co.jp/jp/corc/ir/data/tes/2011/pdf/nr20111019.pdf

�P�DFA�ւ̕�V�ɂ���

�����z�ɑ��ĂT���̐�����V�܂ł͑Ó����Ǝv�����ǁA���̉��̊��������������B

�O�W�N�F���{�Q������]����FA�Ɋ������P�D�W���h���Ŕ��p

�P�O�N�F�o�c���j����P�O�O���q��Ђɂ��邱�Ƃɂ��ĂU�D�Q���h���Ŋ����w��

�E�E�E�E���ق��B

�Q�D�R�Ђ̔����ɂ���

�e�ЂƂ��A�N�Ԕ���グ�͂P-�Q���̉�ЁB����ɉ��Ŋe�Q�O�O�����o�����H

�������A������S�����x����ЂŔ����̐��N�O�Ɍ��̋ƑԂƂ͕ʂ̋ƑԂŊ������ĊJ������ƁB

�E�E�E�E���肫���肷����B���肫���肷�����I�����p�X�B

����ɁA�ꕔ�ɂ��ƁA�R���ׂẲ�Ђ̊��������Ă�p�Г�����Ђ�����Ƃ��i�R�c�s���j

�R�DFA�ɂ���

�v�U�O�O���~�x������FA�̎��������J���Ă���Ȍ��������ˁ[��w

�Ǘ��|�X�g���ꂷ��Ƃ��̃J�X��Ђ̎��ƕɂ͂Ƃ��Ă��悭����b���ˁB

�i�����I�ɂ͂��Ԃ�e�삪�j�Ȃ�炩���Ăǂ����̍��̋��Z�}�t�B�A�ɐH�����ꂽ�̂�

���Ԃ�ԈႢ�Ȃ��Ǝv���B�����A�P�Q�O�O�����炢�ł̏������Ó����Ɣ��f����ɑ��闝�R��

����\���������ŁA����ȏ�͔��f�ۗ��B

�P�DFA�ւ̕�V�ɂ���

�����z�ɑ��ĂT���̐�����V�܂ł͑Ó����Ǝv�����ǁA���̉��̊��������������B

�O�W�N�F���{�Q������]����FA�Ɋ������P�D�W���h���Ŕ��p

�P�O�N�F�o�c���j����P�O�O���q��Ђɂ��邱�Ƃɂ��ĂU�D�Q���h���Ŋ����w��

�E�E�E�E���ق��B

�Q�D�R�Ђ̔����ɂ���

�e�ЂƂ��A�N�Ԕ���グ�͂P-�Q���̉�ЁB����ɉ��Ŋe�Q�O�O�����o�����H

�������A������S�����x����ЂŔ����̐��N�O�Ɍ��̋ƑԂƂ͕ʂ̋ƑԂŊ������ĊJ������ƁB

�E�E�E�E���肫���肷����B���肫���肷�����I�����p�X�B

����ɁA�ꕔ�ɂ��ƁA�R���ׂẲ�Ђ̊��������Ă�p�Г�����Ђ�����Ƃ��i�R�c�s���j

�R�DFA�ɂ���

�v�U�O�O���~�x������FA�̎��������J���Ă���Ȍ��������ˁ[��w

�Ǘ��|�X�g���ꂷ��Ƃ��̃J�X��Ђ̎��ƕɂ͂Ƃ��Ă��悭����b���ˁB

�i�����I�ɂ͂��Ԃ�e�삪�j�Ȃ�炩���Ăǂ����̍��̋��Z�}�t�B�A�ɐH�����ꂽ�̂�

���Ԃ�ԈႢ�Ȃ��Ǝv���B�����A�P�Q�O�O�����炢�ł̏������Ó����Ɣ��f����ɑ��闝�R��

����\���������ŁA����ȏ�͔��f�ۗ��B

25 �F���o�Â鏈�̖������F2011/10/22(�y) 23:15:14.62 ID:QqV3H5rt

26 �F���o�Â鏈�̖������F2011/10/22(�y) 23:41:03.78 ID:8NkF6g2p

>>22

������������

������������

27 �F���o�Â鏈�̖������F2011/10/23(��) 00:32:57.61 ID:zpIdB3w+

28 �F���o�Â鏈�̖������F2011/10/23(��) 00:57:45.04 ID:ZLMKxJgC

����͂܂�������ƃA���ȂƂ�������鏑�����Ȃ̂�����ǁA�Đ��\�G�l���M�[�ɂ��āA�����̓������c�_�����Ă�����̂Ȃ̂ŁE�E

--------------------------------------------------------------------------------------------------------------------------

ttp://theenergycollective.com/willem-post/67528/german-nuclear-decommissioning-and-renewables-build-out

German Nuclear Decommissioning and Renewables Build-Out

�h�C�c�̒E�����ƍĐ��\�G�l���M�[�U���ɂ��Ă̕���

�h�C�c���{�����\���Ă���G�l���M�[����̍��ƖڕW�Ƃ����̂������āF

RENEWABLE ENERGY AND ENERGY EFFICIENCY TARGETS

In September 2010 the German government announced the following targets:

�i1�jRenewable electricity - 35% by 2020 and 80% by 2050�@�@���d�̃G�l���M�[�\�[�X��2020�N��35���Đ��\�G�l���M�[�ɁA2050�N��80����

�i2�jRenewable energy - 18% by 2020, 30% by 2030, and 60% by 2050�@���G�l���M�[���v�̍Đ��\�G�l���M�[�䗦���A2020�N��18���A2030�N��30���A2050�N��60����

�i3�jEnergy efficiency - Reducing the national electricity consumption 50% below 2008 levels by 2050�@2050�N�܂łɓd�͏����2008�N�̔���

�ȉ���

���̕����ł́A��������3�̍��ƖڕW����������ׂ̌v��ƃR�X�g�̊T�Z���q�ׂĂ���B�h�C�c�̏ꍇ�A�Đ��\�G�l���M�[�̎���͕��͔��d

�i�嗤�̐��[�Ȃ̂Ŗk���h�C�c�ɂ͍P��I�ȕΐ���������j������I�t�V���A�i�����̊C���ł̕��͔��d�j�����C���ɂȂ�B�o�C�I�}�X���d��

���͔��d�����͂̔������x�ő��z�����d�͕��͂̎O���̈���x

�h�C�c�̒E�����E�Đ��\�G�l���M�[�ւ̓]���Ƃ����̂́i3�j�̖ڕW�̑�_�ȏȃG�l�ƃZ�b�g�ɂȂ��Ă���B�ȃG�l�ɂ��d�͎��v���Ɍ�

�炵�āA���̓d�͂������Ȃ��ɘd���Ƃ������́B���̂��߂ɁA���̏ȃG�l�A�d�͎��v��l�߂��A�ǂ̒��x�\�E�K�v�Ȃ̂��Ƃ����c�_��������

According to The Breakthrough Institite, Germany would have to reduce its total electricity consumption by about 22% of current 2020

projections AND achieve its target for 35% electricity generated from renewables by 2020. This would require increased energy

efficiency measures to effect an average annual decrease of the electricity consumption/GDP ratio of 3.92% per year, significantly

greater than the 1.47% per year decrease assumed by the IEA's BAU forecasts which is based on projected German GDP growth and current

German efficiency policies.

�V���N�^���N��Breakthrough Institite�̌v�Z�ł͓d�͎��v�̍팸��2020�N��22���̍팸�ł���K�v������A����Ɠ����ɍĐ��\�G�l���M�[��

���d��2020�N�܂ł�35������������K�v������B�����GDP������̔N���̌�������̔䗦�Ō���ƁA���N3.92���̌�������ɂȂ���IEA���h�C�c

�ɂ��Ď��Z����1.47��������ϑ傫��

���d�͎��v�̑啝�팸�Ƃ����͎̂Y�ƃZ�N�^�[�̏ȃG�l�݂̂Ȃ炸�f�M�Z��Ȃǂɂ��Z���̒g�[��[�p�̃G�l���M�[�̐ߖ�Ȃǂɂ��Ƃ��Ă���B

�Đ��\�G�l���M�[�ւ̓����R�X�g�T�Z���݂Ă��A���̕����ł͓d�͗����͍������̂ɂ肻���Ȏ����z���ł��ċ����[�����̂��E�E

--------------------------------------------------------------------------------------------------------------------------

ttp://theenergycollective.com/willem-post/67528/german-nuclear-decommissioning-and-renewables-build-out

German Nuclear Decommissioning and Renewables Build-Out

�h�C�c�̒E�����ƍĐ��\�G�l���M�[�U���ɂ��Ă̕���

�h�C�c���{�����\���Ă���G�l���M�[����̍��ƖڕW�Ƃ����̂������āF

RENEWABLE ENERGY AND ENERGY EFFICIENCY TARGETS

In September 2010 the German government announced the following targets:

�i1�jRenewable electricity - 35% by 2020 and 80% by 2050�@�@���d�̃G�l���M�[�\�[�X��2020�N��35���Đ��\�G�l���M�[�ɁA2050�N��80����

�i2�jRenewable energy - 18% by 2020, 30% by 2030, and 60% by 2050�@���G�l���M�[���v�̍Đ��\�G�l���M�[�䗦���A2020�N��18���A2030�N��30���A2050�N��60����

�i3�jEnergy efficiency - Reducing the national electricity consumption 50% below 2008 levels by 2050�@2050�N�܂łɓd�͏����2008�N�̔���

�ȉ���

���̕����ł́A��������3�̍��ƖڕW����������ׂ̌v��ƃR�X�g�̊T�Z���q�ׂĂ���B�h�C�c�̏ꍇ�A�Đ��\�G�l���M�[�̎���͕��͔��d

�i�嗤�̐��[�Ȃ̂Ŗk���h�C�c�ɂ͍P��I�ȕΐ���������j������I�t�V���A�i�����̊C���ł̕��͔��d�j�����C���ɂȂ�B�o�C�I�}�X���d��

���͔��d�����͂̔������x�ő��z�����d�͕��͂̎O���̈���x

�h�C�c�̒E�����E�Đ��\�G�l���M�[�ւ̓]���Ƃ����̂́i3�j�̖ڕW�̑�_�ȏȃG�l�ƃZ�b�g�ɂȂ��Ă���B�ȃG�l�ɂ��d�͎��v���Ɍ�

�炵�āA���̓d�͂������Ȃ��ɘd���Ƃ������́B���̂��߂ɁA���̏ȃG�l�A�d�͎��v��l�߂��A�ǂ̒��x�\�E�K�v�Ȃ̂��Ƃ����c�_��������

According to The Breakthrough Institite, Germany would have to reduce its total electricity consumption by about 22% of current 2020

projections AND achieve its target for 35% electricity generated from renewables by 2020. This would require increased energy

efficiency measures to effect an average annual decrease of the electricity consumption/GDP ratio of 3.92% per year, significantly

greater than the 1.47% per year decrease assumed by the IEA's BAU forecasts which is based on projected German GDP growth and current

German efficiency policies.

�V���N�^���N��Breakthrough Institite�̌v�Z�ł͓d�͎��v�̍팸��2020�N��22���̍팸�ł���K�v������A����Ɠ����ɍĐ��\�G�l���M�[��

���d��2020�N�܂ł�35������������K�v������B�����GDP������̔N���̌�������̔䗦�Ō���ƁA���N3.92���̌�������ɂȂ���IEA���h�C�c

�ɂ��Ď��Z����1.47��������ϑ傫��

���d�͎��v�̑啝�팸�Ƃ����͎̂Y�ƃZ�N�^�[�̏ȃG�l�݂̂Ȃ炸�f�M�Z��Ȃǂɂ��Z���̒g�[��[�p�̃G�l���M�[�̐ߖ�Ȃǂɂ��Ƃ��Ă���B

�Đ��\�G�l���M�[�ւ̓����R�X�g�T�Z���݂Ă��A���̕����ł͓d�͗����͍������̂ɂ肻���Ȏ����z���ł��ċ����[�����̂��E�E

29 �F���o�Â鏈�̖������F2011/10/23(��) 00:59:05.82 ID:ZLMKxJgC

���h�C�c�̍Đ��\�G�l���M�[�ւ̌X�͒n�����g���j�~��Co2�팸�^���ƘA�����Ă���̂�����ǁA���̕����Ɉ˂�Ε��͔��d�ł�Co2�팸�͂ł�

�Ȃ��Ƃ����B���͔��d�̔��d�ʂ̕p�ɂȕϓ���₤���߂ɁA�o�͒����̗e�ՂȃK�X�^�[�r�����d�ŕ�����������̂�����ǁA���������100�|200��

�̃I���I�t���J��Ԃ��悤�ȉ^�p�ł͔R������͍ň���Co2�r�o��������̂��Ƃ���

Wind and Solar Energy Depend on Gas: Wind and solar energy is variable and intermittent. This requires quick-ramping gas turbine plants

to operate at part-load and quickly ramp up with wind energy ebbs and quickly ramp down with wind energy surges; this happens about

100 to 200 times a day resulting in increased wear and tear. Such operation is very inefficient for gas turbines causing them to use

extra fuel/kWh and emit extra CO2/kWh that mostly offset the claimed fuel and CO2 reductions due to wind energy.

ttp://theenergycollective.com/willem-post/64492/wind-energy-reduces-co2-emissions-few-percent

�Ȃ��Ƃ����B���͔��d�̔��d�ʂ̕p�ɂȕϓ���₤���߂ɁA�o�͒����̗e�ՂȃK�X�^�[�r�����d�ŕ�����������̂�����ǁA���������100�|200��

�̃I���I�t���J��Ԃ��悤�ȉ^�p�ł͔R������͍ň���Co2�r�o��������̂��Ƃ���

Wind and Solar Energy Depend on Gas: Wind and solar energy is variable and intermittent. This requires quick-ramping gas turbine plants

to operate at part-load and quickly ramp up with wind energy ebbs and quickly ramp down with wind energy surges; this happens about

100 to 200 times a day resulting in increased wear and tear. Such operation is very inefficient for gas turbines causing them to use

extra fuel/kWh and emit extra CO2/kWh that mostly offset the claimed fuel and CO2 reductions due to wind energy.

ttp://theenergycollective.com/willem-post/64492/wind-energy-reduces-co2-emissions-few-percent

30 �F���o�Â鏈�̖������F2011/10/23(��) 01:04:31.21 ID:ZLMKxJgC

>>29

�k���h�C�c�̉����ɕ��͔��d�����݂��A����ȑ��d�Ԃ�����Ă��A�⊮�p�̃K�X�^�[�r�����d�Ɉˑ���������ACo2�r�o������Ȃ�

�̂ł���A�Ȃ�ōĐ��\�G�l���M�[�ɂ������̂��Ƃ����^������܂��Ǝv�ӁB�����������d��p�͑�ύ����Ȃ�킯�ŁE�E

�k���h�C�c�̉����ɕ��͔��d�����݂��A����ȑ��d�Ԃ�����Ă��A�⊮�p�̃K�X�^�[�r�����d�Ɉˑ���������ACo2�r�o������Ȃ�

�̂ł���A�Ȃ�ōĐ��\�G�l���M�[�ɂ������̂��Ƃ����^������܂��Ǝv�ӁB�����������d��p�͑�ύ����Ȃ�킯�ŁE�E

31 �F���o�Â鏈�̖������F2011/10/23(��) 01:09:25.84 ID:+3oubvUR

>>30

���܂ł��u���v�Ƃ�����ŏ�ǂ��ێ������������ł́H

���܂ł��u���v�Ƃ�����ŏ�ǂ��ێ������������ł́H

32 �F���o�Â鏈�̖������F2011/10/23(��) 01:20:05.35 ID:sRtzZTco

����ݾ�͉����Č��\���Ă�Ǝv�����ǁA���R�G�l���M�[�̔��d�͕s����

�i����ݾ�̏ꍇ�͑��z�������C�����ȁH�j�Ȃ̂ł��邪�A�O���t�̎��Ԏ�

�����ԒP�ʂɂ������Ȃ�Ɉ��肵�Č�����B�i��d�����ɐ���`�\����

���x�j

����͕��ς�㩂ł�����臒l������Ȃ玞�ԓ��ł��Z���̒�d�͋N����w

�������萔�S��̋N���ƒ�~�͕��ʂɋN���肦���Ȃ��c

����̓z�b�g�X�|�b�g�������ŁA���ς���Ζ��Ȃ��Ƃ��Ǐ��I�Ɍ���Έُ�

�l�i�s�[�N�l�j�ƌ����͓̂�����O�ɔ��������w

�ł�����͕��ː����l�̂ɉe����^����Ƃ��Ă��A����̓s�[�N�l���͕���

�l�̕������Ȃ낤���ǂ˂��B

�A�x�C���r���e�B�������ł��AMTBF���Z�������ǂ��ꍇ�ƒ��������ǂ��ꍇ��

�����ɑ��݂�����w

�i����ݾ�̏ꍇ�͑��z�������C�����ȁH�j�Ȃ̂ł��邪�A�O���t�̎��Ԏ�

�����ԒP�ʂɂ������Ȃ�Ɉ��肵�Č�����B�i��d�����ɐ���`�\����

���x�j

����͕��ς�㩂ł�����臒l������Ȃ玞�ԓ��ł��Z���̒�d�͋N����w

�������萔�S��̋N���ƒ�~�͕��ʂɋN���肦���Ȃ��c

����̓z�b�g�X�|�b�g�������ŁA���ς���Ζ��Ȃ��Ƃ��Ǐ��I�Ɍ���Έُ�

�l�i�s�[�N�l�j�ƌ����͓̂�����O�ɔ��������w

�ł�����͕��ː����l�̂ɉe����^����Ƃ��Ă��A����̓s�[�N�l���͕���

�l�̕������Ȃ낤���ǂ˂��B

�A�x�C���r���e�B�������ł��AMTBF���Z�������ǂ��ꍇ�ƒ��������ǂ��ꍇ��

�����ɑ��݂�����w

33 �F���o�Â鏈�̖������F2011/10/23(��) 01:35:33.46 ID:s3StIoSe

>>30

�Ȃ�Ō���Ȃ��̂��ȁH���܂����킩���B

�Ȃ�Ō���Ȃ��̂��ȁH���܂����킩���B

34 �F���o�Â鏈�̖������F2011/10/23(��) 01:43:37.65 ID:ZLMKxJgC

ttp://theenergycollective.com/willem-post/64492/wind-energy-reduces-co2-emissions-few-percent

Wind Energy Does Little to Reduce CO2 Emissions�@ Posted September 8, 2011

Wind Energy Does Little to Reduce CO2 Emissions�@ Posted September 8, 2011

35 �F���o�Â鏈�̖������F2011/10/23(��) 01:48:29.36 ID:ZLMKxJgC

ttp://sankei.jp.msn.com/world/news/111023/asi11102300090000-n1.htm

�Z���o���R�N�@���R�S���l�������Ώ��ł����@���ɔ��鐅�@�@2011.10.23 00:04

�o���R�N�ł͗��R�S���l���A��h�̍\�z�A�C����~�������Ȃǂɓ������Ă���B�����A�\���ɑΏ��ł����A�R��l���n���̕������瓊�����ꂽ�B

��R���A�b�P�R�O�A���@�Ŗk���h�����A���n��̊�n�ɁA�n���̕����҂��������ȂǁA�Ή��ɒǂ��Ă���B

���{�̓o���R�N�ɂP�V�S�R�J���̔���݂��A�P�P���l�]������e�����B�h�����A���n��̃h�����A����`�ɂ�������A���̈�B�S�P�U

�S���������������A���^�����ȂǁA�Q���̔�Ў҂P�V�O�O�l����炷�B�g�����o���h�̑O�ɂ͗ł��A�R�ς݂ɂȂ����~���������{�����e�B�A

���i�{�[�����ɋl�ߍ���ł����B

�@�E�E�E

�������B�̎x�������ɂ��ẮA���{����������{�����S�̏����n���Ȃ���v��I�Ɏ��W�A�x�������̂ł͂Ȃ��B�e�Ȓ��⌧�A�^�N�V����

�x���h�Ȃǂ��o���o���ɍs���Ă���A����u�c����v���B�H�ƂȂǂ��������܂ɂ́A�u�C�����b�N�v�Ə����ꂽ��A���ɂ̓^�N�V����

�̊�ʐ^���������肵�����̂�����A�����́u��`�c�[���v�ɂ��Ȃ��Ă���B

�Z���o���R�N�@���R�S���l�������Ώ��ł����@���ɔ��鐅�@�@2011.10.23 00:04

�o���R�N�ł͗��R�S���l���A��h�̍\�z�A�C����~�������Ȃǂɓ������Ă���B�����A�\���ɑΏ��ł����A�R��l���n���̕������瓊�����ꂽ�B

��R���A�b�P�R�O�A���@�Ŗk���h�����A���n��̊�n�ɁA�n���̕����҂��������ȂǁA�Ή��ɒǂ��Ă���B

���{�̓o���R�N�ɂP�V�S�R�J���̔���݂��A�P�P���l�]������e�����B�h�����A���n��̃h�����A����`�ɂ�������A���̈�B�S�P�U

�S���������������A���^�����ȂǁA�Q���̔�Ў҂P�V�O�O�l����炷�B�g�����o���h�̑O�ɂ͗ł��A�R�ς݂ɂȂ����~���������{�����e�B�A

���i�{�[�����ɋl�ߍ���ł����B

�@�E�E�E

�������B�̎x�������ɂ��ẮA���{����������{�����S�̏����n���Ȃ���v��I�Ɏ��W�A�x�������̂ł͂Ȃ��B�e�Ȓ��⌧�A�^�N�V����

�x���h�Ȃǂ��o���o���ɍs���Ă���A����u�c����v���B�H�ƂȂǂ��������܂ɂ́A�u�C�����b�N�v�Ə����ꂽ��A���ɂ̓^�N�V����

�̊�ʐ^���������肵�����̂�����A�����́u��`�c�[���v�ɂ��Ȃ��Ă���B

36 �F���o�Â鏈�̖������F2011/10/23(��) 05:05:10.43 ID:l+1OkD+E

8���o�퍕����6�J���A�������A�f�Վ��x�̐Ԏ��]����

���C�^�[ 10��11��(��)10��23���z�M

http://headlines.yahoo.co.jp/hl?a=20111011-00000594-reu-bus_all

>�f�Վ��x�͂U�X�S�V���~�̐Ԏ��B�Q�O�O�X�N�P���̂W�S�S�W���~�A�Q�O�P�P�N�T���̂V�V�P�R���~�Ɏ����A�ߋ��R�Ԗڂ�

>�Ԏ������L�^�����B�z�����R���̉��i�㏸���ɂ��A���̑������A�o�̑�������ł������A�R�J���Ԃ��

>�Ԏ��ɓ]�������B

���C�^�[ 10��11��(��)10��23���z�M

http://headlines.yahoo.co.jp/hl?a=20111011-00000594-reu-bus_all

>�f�Վ��x�͂U�X�S�V���~�̐Ԏ��B�Q�O�O�X�N�P���̂W�S�S�W���~�A�Q�O�P�P�N�T���̂V�V�P�R���~�Ɏ����A�ߋ��R�Ԗڂ�

>�Ԏ������L�^�����B�z�����R���̉��i�㏸���ɂ��A���̑������A�o�̑�������ł������A�R�J���Ԃ��

>�Ԏ��ɓ]�������B

37 �F���o�Â鏈�̖������F2011/10/23(��) 05:05:43.83 ID:ChX8IJM5

>>33

���͔��d�̔��d�ʂɂ��킹�Ĕ��d�ʕς��Ă邩�炾�낤

�K�X�^�[�r���͒�i�^�]�ł��Ȃ��Ɣ��ɔR�����

�i�A�C�h�����O�ł��S�J���̂T�O���߂��R������ʁj

���ۂ̗Ⴞ�Ƌ쒀�͂Ƃ��̌R�p�͒����K�X�^�[�r���̑���

�ᑬ�i���q�j�p�̃G���W����ʂɐςނ��炢�R�����

���͔��d�̔��d�ʂɂ��킹�Ĕ��d�ʕς��Ă邩�炾�낤

�K�X�^�[�r���͒�i�^�]�ł��Ȃ��Ɣ��ɔR�����

�i�A�C�h�����O�ł��S�J���̂T�O���߂��R������ʁj

���ۂ̗Ⴞ�Ƌ쒀�͂Ƃ��̌R�p�͒����K�X�^�[�r���̑���

�ᑬ�i���q�j�p�̃G���W����ʂɐςނ��炢�R�����

38 �F���o�Â鏈�̖������F2011/10/23(��) 05:20:51.33 ID:5cIPYKdF

>>36

����23�N8���� ���ێ��x�i����j�̊T�v

����23�N10��11��

������

�T�@�o����x

�o����x�F4,075���~�̍����i�O�N�����䁣7,354���~�m��64.3���n�������k���j

�u�������x�v�̍������͊g�債�����̂́A�u�f�ՁE�T�[�r�X���x�v���Ԏ��ɓ]�������Ƃ���A�o����x�̍������͏k�������B�o����x�͖{�N�R������U�����A���̍������k���B

1.�f�ՁE�T�[�r�X���x�F��8,773���~�̐Ԏ��i�O�N�����䁣9,710���~ �Ԏ��ɓ]���j

�u�f�Վ��x�v���Ԏ��ɓ]���A�u�T�[�r�X���x�v�̐Ԏ������g�債�����Ƃ���A�f�ՁE�T�[�r�X���x�͐Ԏ��ɓ]�����B�f�ՁE�T�[�r�X���x�͂Q�����A���̐Ԏ��i�Ԏ����͊�����Q�ʁj�B

(1) �f�Վ��x�F��6,947���~�̐Ԏ��i�O�N�����䁣8,653���~�@�Ԏ��ɓ]���j

�z�����R���̉��i�㏸���ɂ��A���̑������A�o�̑���������A�f�Վ��x�͐Ԏ��ɓ]�����i�O����1,233���~�̍����j�B�f�Վ��x�͖{�N�T���ȗ��R�����Ԃ�̐Ԏ��i�Ԏ����͊�����R�ʁj�B

�@ �A�o�F5��1,063���~�i�O�N������{1,970���~�m�{4.0���n �����j

�O�N�������6�����U��̑����i�O���F��2.3�����j�B

�A �A���F5��8,011���~�i�O�N������{1��623���~�m�{22.4���n �����j

�O�N�������20�����A���̑����i�O���F�{13.6�����j�B

�i1�j �A�o�F5��3,566���~�i�O�N������{1,468���~�m�{2.8���n �����j

�@ �u��v�n��ʁv�ł́A�d�t�i���{351���~ [�{6.0��]�j�A�Εč��i���{272���~ �m�{3.5���n�j�A�Α�m�B�i���{234���~�m�{19.8���n�j�A�A�W�A�i���{103���~�m�{0.3���n�A���������i���{253���~�m�{2.4���n�j���������B

�A �u���i�ʁv�ł́A�D���i���{338���~�m�{35.2���n�j�A�����ԁi���{338���~�m�{5.3���n�j���������B�����A�����̓��d�q���i�i����581���~ [��16.4��]�j���������B

�i2�j �A���F6��1,338���~�i�O�N������{9,878���~�m�{19.2���n �����j

�@ �u��v�n��ʁv�ł́A�Β����i���{4,065���~ �m�{51.6���n�j�A�A�W�A�i���{3,816���~�m�{16.6���n�A���������i���{1,832���~�m�{16.4���n�j�j�A�Α�m�B�i���{968���~�m�{23.4���n�j���������B

�A �u���i�ʁv�ł́A���e���i���{2,944���~�m�{39.9��]�G���ʂ́{1.2��)�A�t���V�R�K�X(���{1,790���~�m�{55.7��]�G���ʂ́{18.2��)���������B�����A�����̓��d�q���i�i����540���~�m��27.7��])���������B

[�Q�l�Q�n �������i�i���A���j

�@�h���x�[�X�F114.59�ăh���^�o�����i�ΑO�N������{53.4���j

�A�~�x�[�X�F56,140�~�^�L�����b�g���i�ΑO�N������{38.3���j

����23�N8���� ���ێ��x�i����j�̊T�v

����23�N10��11��

������

�T�@�o����x

�o����x�F4,075���~�̍����i�O�N�����䁣7,354���~�m��64.3���n�������k���j

�u�������x�v�̍������͊g�債�����̂́A�u�f�ՁE�T�[�r�X���x�v���Ԏ��ɓ]�������Ƃ���A�o����x�̍������͏k�������B�o����x�͖{�N�R������U�����A���̍������k���B

1.�f�ՁE�T�[�r�X���x�F��8,773���~�̐Ԏ��i�O�N�����䁣9,710���~ �Ԏ��ɓ]���j

�u�f�Վ��x�v���Ԏ��ɓ]���A�u�T�[�r�X���x�v�̐Ԏ������g�債�����Ƃ���A�f�ՁE�T�[�r�X���x�͐Ԏ��ɓ]�����B�f�ՁE�T�[�r�X���x�͂Q�����A���̐Ԏ��i�Ԏ����͊�����Q�ʁj�B

(1) �f�Վ��x�F��6,947���~�̐Ԏ��i�O�N�����䁣8,653���~�@�Ԏ��ɓ]���j

�z�����R���̉��i�㏸���ɂ��A���̑������A�o�̑���������A�f�Վ��x�͐Ԏ��ɓ]�����i�O����1,233���~�̍����j�B�f�Վ��x�͖{�N�T���ȗ��R�����Ԃ�̐Ԏ��i�Ԏ����͊�����R�ʁj�B

�@ �A�o�F5��1,063���~�i�O�N������{1,970���~�m�{4.0���n �����j

�O�N�������6�����U��̑����i�O���F��2.3�����j�B

�A �A���F5��8,011���~�i�O�N������{1��623���~�m�{22.4���n �����j

�O�N�������20�����A���̑����i�O���F�{13.6�����j�B

�i1�j �A�o�F5��3,566���~�i�O�N������{1,468���~�m�{2.8���n �����j

�@ �u��v�n��ʁv�ł́A�d�t�i���{351���~ [�{6.0��]�j�A�Εč��i���{272���~ �m�{3.5���n�j�A�Α�m�B�i���{234���~�m�{19.8���n�j�A�A�W�A�i���{103���~�m�{0.3���n�A���������i���{253���~�m�{2.4���n�j���������B

�A �u���i�ʁv�ł́A�D���i���{338���~�m�{35.2���n�j�A�����ԁi���{338���~�m�{5.3���n�j���������B�����A�����̓��d�q���i�i����581���~ [��16.4��]�j���������B

�i2�j �A���F6��1,338���~�i�O�N������{9,878���~�m�{19.2���n �����j

�@ �u��v�n��ʁv�ł́A�Β����i���{4,065���~ �m�{51.6���n�j�A�A�W�A�i���{3,816���~�m�{16.6���n�A���������i���{1,832���~�m�{16.4���n�j�j�A�Α�m�B�i���{968���~�m�{23.4���n�j���������B

�A �u���i�ʁv�ł́A���e���i���{2,944���~�m�{39.9��]�G���ʂ́{1.2��)�A�t���V�R�K�X(���{1,790���~�m�{55.7��]�G���ʂ́{18.2��)���������B�����A�����̓��d�q���i�i����540���~�m��27.7��])���������B

[�Q�l�Q�n �������i�i���A���j

�@�h���x�[�X�F114.59�ăh���^�o�����i�ΑO�N������{53.4���j

�A�~�x�[�X�F56,140�~�^�L�����b�g���i�ΑO�N������{38.3���j

39 �F���o�Â鏈�̖������F2011/10/23(��) 05:22:43.58 ID:5cIPYKdF

>>38����

(2) �T�[�r�X���x�F��1,826���~�̐Ԏ��i�O�N�����䁣1,057���~�@�Ԏ����g��j

�u���̑��c���Ɩ��i����f�Վ萔�����̎�挸�j�v���Ԏ��ɓ]���A�u���s���x�v�̐Ԏ������g�債�����Ɠ��ɂ��A�T�[�r�X���x�̐Ԏ�����3�����A���Ŋg�債���B

[�Q�l�R�n �K���O���l���s�Ґ��F546,800�l�i�ΑO�N�����䁣31.9���j

�@�@�@�@�@ �o�����{�l���F1,792,000�l�i�ΑO�N������{9.1���j

�i�o�T�F���{���{�ό���(JNTO)�j

2.�������x�F1��3,539���~�̍����i�O�N������{2,089���~�m�{18.2��] �������g��j

�،������ɌW��z�����̎�摝��������Ƃ��āA�������x�̍�������5�����A���Ŋg�債���B

http://www.mof.go.jp/international_policy/reference/balance_of_payments/preliminary/pg2308.htm

(�Q�l)�o����x�̐��ځ@�G�ߒ�����

http://www.mof.go.jp/international_policy/reference/balance_of_payments/preliminary/bpgaiyou1108b.GIF

(2) �T�[�r�X���x�F��1,826���~�̐Ԏ��i�O�N�����䁣1,057���~�@�Ԏ����g��j

�u���̑��c���Ɩ��i����f�Վ萔�����̎�挸�j�v���Ԏ��ɓ]���A�u���s���x�v�̐Ԏ������g�債�����Ɠ��ɂ��A�T�[�r�X���x�̐Ԏ�����3�����A���Ŋg�債���B

[�Q�l�R�n �K���O���l���s�Ґ��F546,800�l�i�ΑO�N�����䁣31.9���j

�@�@�@�@�@ �o�����{�l���F1,792,000�l�i�ΑO�N������{9.1���j

�i�o�T�F���{���{�ό���(JNTO)�j

2.�������x�F1��3,539���~�̍����i�O�N������{2,089���~�m�{18.2��] �������g��j

�،������ɌW��z�����̎�摝��������Ƃ��āA�������x�̍�������5�����A���Ŋg�債���B

http://www.mof.go.jp/international_policy/reference/balance_of_payments/preliminary/pg2308.htm

(�Q�l)�o����x�̐��ځ@�G�ߒ�����

http://www.mof.go.jp/international_policy/reference/balance_of_payments/preliminary/bpgaiyou1108b.GIF

{kind=link}

40 �F���o�Â鏈�̖������F2011/10/23(��) 05:23:33.84 ID:l+1OkD+E

�ڍׂ��肪�ƁB

�ł��O�X���I�Ղɂ������u�f�Վ��x�̐Ԏ����Č������ƂȂ��v�Ƃ����J�L�R�ɂ������āA����Ȃ��ƂȂ����Ƃ���

����ŃR�s�y�������������炗

�ł��O�X���I�Ղɂ������u�f�Վ��x�̐Ԏ����Č������ƂȂ��v�Ƃ����J�L�R�ɂ������āA����Ȃ��ƂȂ����Ƃ���

����ŃR�s�y�������������炗

41 �F���o�Â鏈�̖������F2011/10/23(��) 05:40:09.58 ID:5KZDkZj6

>>11

�g���R��D���Ȃ́H�悯���������

�g���R��D���Ȃ́H�悯���������

42 �F���o�Â鏈�̖������F2011/10/23(��) 05:58:23.62 ID:5cIPYKdF

>>40

�f�Վ��x���o����x�����x�������ɂ͎��X�Ԏ��ɂȂ��Ă邩���

���Ԃ�80�N��ȍ~�Ȃ�Ԏ��͂Ȃ������Ǝv��

���̂Ƃ���͌������i�㏸�ƌ�����~�A�A�o�̐L�т̓݉��A�O���l���s�Ҍ��ȂǂŁA

�f�Վ��x�͐Ԏ��ɂȂ��Ă��

�܂��������x���傫���̂Ōo����x�͂܂������������Ă邯��

�f�Վ��x���o����x�����x�������ɂ͎��X�Ԏ��ɂȂ��Ă邩���

���Ԃ�80�N��ȍ~�Ȃ�Ԏ��͂Ȃ������Ǝv��

���̂Ƃ���͌������i�㏸�ƌ�����~�A�A�o�̐L�т̓݉��A�O���l���s�Ҍ��ȂǂŁA

�f�Վ��x�͐Ԏ��ɂȂ��Ă��

�܂��������x���傫���̂Ōo����x�͂܂������������Ă邯��

43 �F���o�Â鏈�̖������F2011/10/23(��) 06:42:57.42 ID:ZLMKxJgC

�g���R�̐����^�}��G���h�A���̐l�C�������A�����̎x���������āA��}��R���ɂ͎肪�o���Ȃ��ő�̗��R�́A���̂Ƃ���

�����Ă���o�ς̍D���ł��傤�˂�

ttp://www.invest.gov.tr/ja-JP/infocenter/news/Pages/301110-turkish-economy-betters-competitors-deloitte.aspx

�f���C�g:�g���R�o�ς͐��E�̌o�Ϗ�E���� 30.11.2010

�����Ă���o�ς̍D���ł��傤�˂�

ttp://www.invest.gov.tr/ja-JP/infocenter/news/Pages/301110-turkish-economy-betters-competitors-deloitte.aspx

�f���C�g:�g���R�o�ς͐��E�̌o�Ϗ�E���� 30.11.2010

44 �F���o�Â鏈�̖������F2011/10/23(��) 06:44:46.44 ID:C7/5lxCq

���B�A���̗��O�ɍ���畴���K�����끃�g���R

45 �F���o�Â鏈�̖������F2011/10/23(��) 07:01:12.96 ID:ZLMKxJgC

ttp://www.47news.jp/CN/201110/CN2011102201000839.html

�����_���A���q�͋���̏��F�v���@�s�Ȃ���{��ƑI���@2011/10/23 02:02 �y�����ʐM�z

���{�ƃ����_���������������q�͕��a���p��������Ɍ������{�̍���F��N���܂łɏI����悤�����_�����{���������{���{�ɋ����v������

�������Ƃ��Q�Q���A���������B�����_�����������v��̔������N���Ɍ��߂邽�߂ŁA�s�\�ȏꍇ�͖@�I��������Ȃ��Ƃ��ē��{�̊��

�͑I�肵�Ȃ��Ǝ�����A�ʍ����Ă���B�����̊O�������炩�ɂ����B

�����d�͕�����P�������̂��A�����A�o�ɂȂ��鋦�蔭���ɂ͗^��}���ŐT�d�E���Θ_���������A��c���F�͓���Ή��𔗂�ꂻ�����B

�����_���A���q�͋���̏��F�v���@�s�Ȃ���{��ƑI���@2011/10/23 02:02 �y�����ʐM�z

���{�ƃ����_���������������q�͕��a���p��������Ɍ������{�̍���F��N���܂łɏI����悤�����_�����{���������{���{�ɋ����v������

�������Ƃ��Q�Q���A���������B�����_�����������v��̔������N���Ɍ��߂邽�߂ŁA�s�\�ȏꍇ�͖@�I��������Ȃ��Ƃ��ē��{�̊��

�͑I�肵�Ȃ��Ǝ�����A�ʍ����Ă���B�����̊O�������炩�ɂ����B

�����d�͕�����P�������̂��A�����A�o�ɂȂ��鋦�蔭���ɂ͗^��}���ŐT�d�E���Θ_���������A��c���F�͓���Ή��𔗂�ꂻ�����B

46 �F���o�Â鏈�̖������F2011/10/23(��) 07:14:32.72 ID:ZLMKxJgC

ttp://blogs.wsj.com/marketbeat/2011/10/21/eurozone-summits-what-to-watch-for/?mod=WSJBlog

Eurozone Summits: What to Watch For�@�@Tom Lauricella

���[�����T�~�b�g�̒��ړ_�i�s��̌����j�@�@�v�r�i�}�[�P�b�g�r�[�g�@OCTOBER 21, 2011, 5:20 PM ET

��Greek debt write down.

Bottom line: Writing down Greek debt needs to be on the table. Public reports have pegged the required haircut at 40-60%. We believe

anything significantly less than this would be a disappointment to the markets.�@

�@�w�A�J�b�g40�|60����\�z�A���Ȃ��Ȃ�s�ꂪ���]

��European bank recapitalization.

Bottom line: Recapitalizing European banks needs to be on the table, since it is directly linked to any credible haircutting of Greece

sovereign debt values. A recapitalization of less than ?70 billion would likely be a disappointment, while ?150 billion or more would

likely be considered to be a credible response.

�@���B��s�̎��{�����A700�����[���ȉ��Ȃ�s��͎��]�A1500�����[���ȏ�Ȃ�[��

��Anti-contagion fund.

Bottom line: Preventing contagion to Spain and Italy needs to be on the table. There are many complex legal issues that surround the

various plans considered to achieve this end. Nearly all of these plans involve leveraging the fund�fs resources either directly or via

the ECB. The plan reported to have the greatest traction involves the fund providing loss insurance to buyers of sovereign bonds in the

secondary market. Rather than engage in a discussion of the pros and cons of the various proposals, we will remain focused on the

overall size of the anti-contagion program. By whatever mechanism policymakers come up with to leverage the EFSF, we think ?2 trillion

is the minimum required to control contagion. An amount less than ?1.5 trillion would likely be viewed as a disappointment.

�@EFSF��2�����[���K�v�A1.5�����[���ȉ��Ȃ�s��͎��]

Eurozone Summits: What to Watch For�@�@Tom Lauricella

���[�����T�~�b�g�̒��ړ_�i�s��̌����j�@�@�v�r�i�}�[�P�b�g�r�[�g�@OCTOBER 21, 2011, 5:20 PM ET

��Greek debt write down.

Bottom line: Writing down Greek debt needs to be on the table. Public reports have pegged the required haircut at 40-60%. We believe

anything significantly less than this would be a disappointment to the markets.�@

�@�w�A�J�b�g40�|60����\�z�A���Ȃ��Ȃ�s�ꂪ���]

��European bank recapitalization.

Bottom line: Recapitalizing European banks needs to be on the table, since it is directly linked to any credible haircutting of Greece

sovereign debt values. A recapitalization of less than ?70 billion would likely be a disappointment, while ?150 billion or more would

likely be considered to be a credible response.

�@���B��s�̎��{�����A700�����[���ȉ��Ȃ�s��͎��]�A1500�����[���ȏ�Ȃ�[��

��Anti-contagion fund.

Bottom line: Preventing contagion to Spain and Italy needs to be on the table. There are many complex legal issues that surround the

various plans considered to achieve this end. Nearly all of these plans involve leveraging the fund�fs resources either directly or via

the ECB. The plan reported to have the greatest traction involves the fund providing loss insurance to buyers of sovereign bonds in the

secondary market. Rather than engage in a discussion of the pros and cons of the various proposals, we will remain focused on the

overall size of the anti-contagion program. By whatever mechanism policymakers come up with to leverage the EFSF, we think ?2 trillion

is the minimum required to control contagion. An amount less than ?1.5 trillion would likely be viewed as a disappointment.

�@EFSF��2�����[���K�v�A1.5�����[���ȉ��Ȃ�s��͎��]

47 �F���o�Â鏈�̖������F2011/10/23(��) 08:05:33.05 ID:bkI5zsG2

8�����ȍ~�ɓ˓��ƂȂ�ƁA

�����A�ʉ߁H

�h�C�c�q�� �W�����ȍ~������

http://www3.nhk.or.jp/news/html/20111023/t10013444621000.html

�����Ȋw�� MEXT

http://www.facebook.com/photo.php?fbid=289176117774145&set=pu.208566032501821&type=1&theater

�����A�ʉ߁H

�h�C�c�q�� �W�����ȍ~������

http://www3.nhk.or.jp/news/html/20111023/t10013444621000.html

�����Ȋw�� MEXT

http://www.facebook.com/photo.php?fbid=289176117774145&set=pu.208566032501821&type=1&theater

48 �F���o�Â鏈�̖������F2011/10/23(��) 08:53:16.63 ID:5KZDkZj6

>>43

���킠��

�Ȃ����L���̃��O�������ė��Ȃ��̂ꂷ�B�B�B

�G���h�A���i�A�Ƃ������A��������"��"�A�ɋ߂����ł����j�̎x������

�����̏��ȂƂ��A�R�������������Ƃ̐����s�����̉����Ƃ��A�߂�����m��Ă���������������

>>44

���B���O�ɍ���Ȃ��Ƃ���́A�����Ɛ����Ă��T�͏o�Ă��邭�炢�AEU�����͉������ꂷ��

���̑���ȃC���t���Ǝ����i�����A�ǂ��N���A���Đ�D���ɂȂꂽ�̂��S������܂��B

>>45

�����_���͕����s�R�����A�ߗׂƂ̌��ˍ������傫���悤�Ɏv���܂��B

�V���A�����ł̊O�������A������s�\�ɋ߂��̂ŃA���u���E�̗͊w�̂��傫�����ƁB

�g���R�̌���m��Ă������������I�I

�����������H�����A�������Ƃ���

���킠��

�Ȃ����L���̃��O�������ė��Ȃ��̂ꂷ�B�B�B

�G���h�A���i�A�Ƃ������A��������"��"�A�ɋ߂����ł����j�̎x������

�����̏��ȂƂ��A�R�������������Ƃ̐����s�����̉����Ƃ��A�߂�����m��Ă���������������

>>44

���B���O�ɍ���Ȃ��Ƃ���́A�����Ɛ����Ă��T�͏o�Ă��邭�炢�AEU�����͉������ꂷ��

���̑���ȃC���t���Ǝ����i�����A�ǂ��N���A���Đ�D���ɂȂꂽ�̂��S������܂��B

>>45

�����_���͕����s�R�����A�ߗׂƂ̌��ˍ������傫���悤�Ɏv���܂��B

�V���A�����ł̊O�������A������s�\�ɋ߂��̂ŃA���u���E�̗͊w�̂��傫�����ƁB

�g���R�̌���m��Ă������������I�I

�����������H�����A�������Ƃ���

49 �F���o�Â鏈�̖������F2011/10/23(��) 08:57:47.64 ID:KixozzUq

�Ԏ��_�̃u���O����BTPP�̑S�e���I�[�v���ɂȂ��������ł���B

�� ���푈 TPP�ƃ}�X�R�~

http://ameblo.jp/takaakimitsuhashi/entry-11056077285.html

�s�o�o������̕���ʏ�

http://www.npu.go.jp/policy/policy08/pdf/20111014/20111021_1.pdf

�� ���푈 TPP�ƃ}�X�R�~

http://ameblo.jp/takaakimitsuhashi/entry-11056077285.html

�s�o�o������̕���ʏ�

http://www.npu.go.jp/policy/policy08/pdf/20111014/20111021_1.pdf

50 �F���o�Â鏈�̖������F2011/10/23(��) 10:45:24.22 ID:vosbP5II

>>48

�����͒������̊w�҂���̃R����

http://www.tkfd.or.jp/blog/sasaki/

�����͊O��̊w�������������Ă�L����|�Ă���T�C�g

http://www.el.tufs.ac.jp/prmeis/news_j.html

���̕ӂ�����ƁA�����̎���͂悭����܂��B

�����͒������̊w�҂���̃R����

http://www.tkfd.or.jp/blog/sasaki/

�����͊O��̊w�������������Ă�L����|�Ă���T�C�g

http://www.el.tufs.ac.jp/prmeis/news_j.html

���̕ӂ�����ƁA�����̎���͂悭����܂��B

51 �F���o�Â鏈�̖������F2011/10/23(��) 11:24:24.53 ID:wZzfMEM8

>>48

�g���R�͂���EU�ɂ͖������Ȃ��Ƃ������Ȃ��B

�g���R�̌���ɂ��Ắi���{�ꎑ���͗]��Ȃ��Ǝv���j�A

Step Up to the Plate

ttp://www.thedailybeast.com/newsweek/2010/09/25/zakaria-rising-powers-aren-t-acting-like-it.html

Then consider Turkey. Twenty years ago, it too was perceived as a basket-case economy, dependent on

American largesse, protected by the American security umbrella, and quietly seeking approval from Europe.

It needed the West. But now Turkey has a booming economy, has an increasingly confident democracy, and

is a major regional power. It is growing faster than every European country, and its bonds are safer than

those of many Southern European nations.

���Ƀg���R�B20�N�O�ɂ̓g���R���_�ƍ��Ƃ���č��̊��e���ɗ���č��̖h�q�͂̎P�Ɏ���Ă����B�����ĐÂ���

���[���b�p����̏��F�����߂Ă����B���m��K�v�Ƃ��Ă����̂��B����������g���R�͐����Ȍo�ς��ւ�A�����`�ւ�

���M��[�߂Ă����v�Ȓn��卑�ł���B�ǂ̃��[���b�p���Ƃ����������Ă���A���������̓새�[���b�p���Ƃ̂���

�������S�ł���B

Its foreign policy is becoming not so much Islamic as Ottoman, reestablishing a sphere of influence it had for

400 years. Abdullah Gül, Turkey�fs sophisticated president, explains that while Turkey remains resolutely a part

of the West, it is increasingly influential in the Middle East, Central Asia, and beyond. �gTurkey is becoming a source

of inspiration for other countries in the region,�h he said to me while in New York last week.

�g���R�̊O�𐭍�̓I�X�}���鍑�̂��̂قǃC�X�����I�Ȃ��̂ɂȂ��Ă����ł͂Ȃ����A�鍑��400�N�ԕۂ��Ă����e������

�Ċm��������B�����̗D�G�ȑ哝�̂ł���A�u�h���E�O���́A�g���R�͂��ꂩ������m�̈ꕔ�ł��邱�Ƃ͊ԈႢ�Ȃ����A

�����⒆���A�W�A�����āA����ȊO�̒n��ɂ��e���͂������Ă����Ƃ��Ă���B�u�g���R�͒n����ő����ɂƂ��ăC���X�s���[�V����

�̌��ƂȂ��Ă����̂ł��v�ƁA��T�j���[���[�N�Ŏ��Ɍ���Ă��ꂽ�B

�g���R�͂���EU�ɂ͖������Ȃ��Ƃ������Ȃ��B

�g���R�̌���ɂ��Ắi���{�ꎑ���͗]��Ȃ��Ǝv���j�A

Step Up to the Plate

ttp://www.thedailybeast.com/newsweek/2010/09/25/zakaria-rising-powers-aren-t-acting-like-it.html

Then consider Turkey. Twenty years ago, it too was perceived as a basket-case economy, dependent on

American largesse, protected by the American security umbrella, and quietly seeking approval from Europe.

It needed the West. But now Turkey has a booming economy, has an increasingly confident democracy, and

is a major regional power. It is growing faster than every European country, and its bonds are safer than

those of many Southern European nations.

���Ƀg���R�B20�N�O�ɂ̓g���R���_�ƍ��Ƃ���č��̊��e���ɗ���č��̖h�q�͂̎P�Ɏ���Ă����B�����ĐÂ���

���[���b�p����̏��F�����߂Ă����B���m��K�v�Ƃ��Ă����̂��B����������g���R�͐����Ȍo�ς��ւ�A�����`�ւ�

���M��[�߂Ă����v�Ȓn��卑�ł���B�ǂ̃��[���b�p���Ƃ����������Ă���A���������̓새�[���b�p���Ƃ̂���

�������S�ł���B

Its foreign policy is becoming not so much Islamic as Ottoman, reestablishing a sphere of influence it had for

400 years. Abdullah Gül, Turkey�fs sophisticated president, explains that while Turkey remains resolutely a part

of the West, it is increasingly influential in the Middle East, Central Asia, and beyond. �gTurkey is becoming a source

of inspiration for other countries in the region,�h he said to me while in New York last week.

�g���R�̊O�𐭍�̓I�X�}���鍑�̂��̂قǃC�X�����I�Ȃ��̂ɂȂ��Ă����ł͂Ȃ����A�鍑��400�N�ԕۂ��Ă����e������

�Ċm��������B�����̗D�G�ȑ哝�̂ł���A�u�h���E�O���́A�g���R�͂��ꂩ������m�̈ꕔ�ł��邱�Ƃ͊ԈႢ�Ȃ����A

�����⒆���A�W�A�����āA����ȊO�̒n��ɂ��e���͂������Ă����Ƃ��Ă���B�u�g���R�͒n����ő����ɂƂ��ăC���X�s���[�V����

�̌��ƂȂ��Ă����̂ł��v�ƁA��T�j���[���[�N�Ŏ��Ɍ���Ă��ꂽ�B

52 �F���o�Â鏈�̖������F2011/10/23(��) 11:42:39.08 ID:SvV6dTf0

�g���R�͉����R�����̃M���V���ɉ��B���������������������������B

�t�ɂ��ꂪ����̊�@�Ɋ������܂ꂸ�ɂ��Ƃ�������B

�t�ɂ��ꂪ����̊�@�Ɋ������܂ꂸ�ɂ��Ƃ�������B

53 �F���o�Â鏈�̖������F2011/10/23(��) 12:26:29.12 ID:BPtbio5e

54 �F���o�Â鏈�̖������F2011/10/23(��) 12:41:10.53 ID:VVRYUQZF

�D���Ƃ������ƁA����EU���A�����J����Ȃ���̂̓g���R���ȁH�ƉA�d�]�������₭w

55 �F���o�Â鏈�̖������F2011/10/23(��) 12:55:18.09 ID:8G4WbtDq

�u���c�������X���̓A�����J�ɏo������v

http://nicoviewer.net/sm14885774

�|���@

�����ō���A�j�b�|���̍����Ƃ��āA�u���c�����ꂽ���{�X���̓A�����J�ɏo������v��

���А\���グ�����B�ŋ߂̃L�[���[�h�A�\�u�����E�E�F���X�E�t�@���h�i�r�v�e�j������܂��B

���{�n�t�@���h�A�܂荑�������Ă������ł��B�A�����J�̋��Z�@�ւ��r�v�e����

�����������P�[�X�������Ă��܂����A����ŁA�������{���玑��������Ă�

�悢�̂��Ƃ�����肪����B���{�ɂ͂��ĂƂ�ł��Ȃ�����Ȃr�v�e������܂����B

���ꂪ���̓��{�X���Ȃ�ł��B�����ʂł�����300���~�B���̂r�v�e�Ƃ�

��ו��ɂȂ�Ȃ��قǂ̂r�v�e����������ł��B���c�������̂ŁA���͂r�v�e�ł͂Ȃ��B

������A�����J���猩��ƈ��S���Ď������A���Ԃ̎����Ȃ�ł��B

�A�����J�ɑ��Ă��v���ł��邵�A�����ɓ��{�X�����猩�Ă��A�A�����J�̋��Z�@�ւ�

�o�����邱�ƂŁA���낢��ȃm�E�n�E��~�ς��A�V���ȃr�W�l�X�ւ̊�b���ł���B

http://blogimg.goo.ne.jp/user_image/35/fa/973a35c2a0067e607500f7e35b6c27cf.jpg

{kind=link}

http://diamond.jp/articles/-/3646?page=3

http://i248.photobucket.com/albums/gg164/rivet_blog/koizumi1.jpg

{kind=link}

http://i248.photobucket.com/albums/gg164/rivet_blog/koizumi2.jpg

{kind=link}

56 �F���o�Â鏈�̖������F2011/10/23(��) 13:06:27.17 ID:iWJYFA5p

>>55

���N�l�ɂƂ��ċ��������f�v��F�߂����Ƃ͎��ʂ܂ŖY����Ȃ����J�Ȃ�w

���N�l�ɂƂ��ċ��������f�v��F�߂����Ƃ͎��ʂ܂ŖY����Ȃ����J�Ȃ�w

57 �F���o�Â鏈�̖������F2011/10/23(��) 13:57:21.11 ID:ZLMKxJgC

ttp://www.bloomberg.co.jp/apps/news?pid=90920012&sid=aNmOS0P3f0E0

�d�t�w���҂͊�@�����Ɍ�����]��c�|��s���{�����ő�10���~���@�@2011/10/23 11:03 JST

�@�@

10��23���i�u���[���o�[�O�j�F���B�A���i�d�t�j�e���̎w���҂�23���A���[������������Ƃd�t������������̌���A�u�����b�Z���ł�

�d�t��]��c�ɗՂށB��]��c��26���ɍēx�J�Â����B

�@�@

26���͇@���B�~�ϊ���̋����A�M���V���̃f�t�H���g�i���s���s�j��������Ȃ��瓯�������팸����B����@�̉e���������̋�s����

��A�C�^���A��X�y�C�������e���Ɋ������Ȃ��悤�m���ɂ���|�Ƃ̂R�̌v����������邽�߂Ɏ���ۂ��������ƂȂ�B

�������̑�ɂ͉��B���Z����t�@�V���e�B�[�i�d�e�r�e�j�ƍP�v�I�ȋ~�Ϙg�g�݂ł��鉢�B���艻���J�j�Y���i�d�r�l�j�����A����̋K

�͂��ő�9400�����[���i��99��6500���~�j�Ƃ��邱�Ƃ�A�M���V�����̕]�����̊g��A��s�̋��`�̒��j�I���Ȏ��{�䗦��2012�N���܂ł�

�X���ֈ����グ�邱�Ƃ��܂܂�Ă���B

�@�@

�d�t�������͉��B�̋�s���\�u�����̎����]����ɖ�1000�����[���i��10��6000���~�j�̎��Ȏ��{�������K�v�ƂȂ�\��������Ƃ̓_�ň�

������v�B�d�t������������̋c�_�ɏڂ����W�҂P�l�����炩�ɂ������̂ŁA���B��s�ē@�\�i�d�a�`�j�̎��Z�Ɋ�Â��ƁA���`�̒��j�I

���Ȏ��{�ł���R�A�s�������P�䗦�łX����B�����邽�߂ɂ��̋��z���K�v�ƂȂ�B

�I�Y�{�[���p�������͉�c�I����ɋL�Ғc�ɑ��A�u�����͎��ۂɑO�i���A���B�̋�s�̋����ŏd�v�Ȍ���ɓ��B�����v�ƌ�����B������

�����Ɂu����͕��̈ꕔ�ł����Ȃ��A��i�̍�Ƃ��K�v�Ȃ͖̂������v�Əq�ׂ��B

�@�@

�܂��A����ɏڂ����W�҂ɂ��ƁA���B�e���̍������͍�����ɋꂵ�ރ��[���������̍��𓊎��Ƃɍw�����Ă��炤����ݗ��ɂ��ċ��c

�����B����ɉ����āA�d�e�r�e�����p���č��ۏ��s�����Ƃ��������ꂽ�B

�d�t�w���҂͊�@�����Ɍ�����]��c�|��s���{�����ő�10���~���@�@2011/10/23 11:03 JST

�@�@

10��23���i�u���[���o�[�O�j�F���B�A���i�d�t�j�e���̎w���҂�23���A���[������������Ƃd�t������������̌���A�u�����b�Z���ł�

�d�t��]��c�ɗՂށB��]��c��26���ɍēx�J�Â����B

�@�@

26���͇@���B�~�ϊ���̋����A�M���V���̃f�t�H���g�i���s���s�j��������Ȃ��瓯�������팸����B����@�̉e���������̋�s����

��A�C�^���A��X�y�C�������e���Ɋ������Ȃ��悤�m���ɂ���|�Ƃ̂R�̌v����������邽�߂Ɏ���ۂ��������ƂȂ�B

�������̑�ɂ͉��B���Z����t�@�V���e�B�[�i�d�e�r�e�j�ƍP�v�I�ȋ~�Ϙg�g�݂ł��鉢�B���艻���J�j�Y���i�d�r�l�j�����A����̋K

�͂��ő�9400�����[���i��99��6500���~�j�Ƃ��邱�Ƃ�A�M���V�����̕]�����̊g��A��s�̋��`�̒��j�I���Ȏ��{�䗦��2012�N���܂ł�

�X���ֈ����グ�邱�Ƃ��܂܂�Ă���B

�@�@

�d�t�������͉��B�̋�s���\�u�����̎����]����ɖ�1000�����[���i��10��6000���~�j�̎��Ȏ��{�������K�v�ƂȂ�\��������Ƃ̓_�ň�

������v�B�d�t������������̋c�_�ɏڂ����W�҂P�l�����炩�ɂ������̂ŁA���B��s�ē@�\�i�d�a�`�j�̎��Z�Ɋ�Â��ƁA���`�̒��j�I

���Ȏ��{�ł���R�A�s�������P�䗦�łX����B�����邽�߂ɂ��̋��z���K�v�ƂȂ�B

�I�Y�{�[���p�������͉�c�I����ɋL�Ғc�ɑ��A�u�����͎��ۂɑO�i���A���B�̋�s�̋����ŏd�v�Ȍ���ɓ��B�����v�ƌ�����B������

�����Ɂu����͕��̈ꕔ�ł����Ȃ��A��i�̍�Ƃ��K�v�Ȃ͖̂������v�Əq�ׂ��B

�@�@

�܂��A����ɏڂ����W�҂ɂ��ƁA���B�e���̍������͍�����ɋꂵ�ރ��[���������̍��𓊎��Ƃɍw�����Ă��炤����ݗ��ɂ��ċ��c

�����B����ɉ����āA�d�e�r�e�����p���č��ۏ��s�����Ƃ��������ꂽ�B

58 �F���o�Â鏈�̖������F2011/10/23(��) 13:58:56.96 ID:ZLMKxJgC

ttp://www.bloomberg.co.jp/apps/news?pid=90920012&sid=aALQ.ykjhYoY

�h�h�e�F�M���V�����ۗL�҂Ƃd�t�̋��c�́u����I�Ȃ���i�W�v�@2011/10/23 11:31 JST

�@�@

10��22���i�u���[���o�[�O�j�F��s�ƊE���\���鍑�ۋ��Z����i�h�h�e�j��22���A�M���V�����̖��ԓ����Ƃ̑������S�g����߂��铊����

�Ɛ������ǎ҂̃u�����b�Z���ł̋��c�ŁA�u����I�v�Ȑi�W�����������Ƃ𖾂炩�ɂ����B�h�h�e�̃_���[���ꖱ�����́u����I�����A�c�_��

�i�W���Ă���v�Ƃ̐����\�����B

�h�h�e�F�M���V�����ۗL�҂Ƃd�t�̋��c�́u����I�Ȃ���i�W�v�@2011/10/23 11:31 JST

�@�@

10��22���i�u���[���o�[�O�j�F��s�ƊE���\���鍑�ۋ��Z����i�h�h�e�j��22���A�M���V�����̖��ԓ����Ƃ̑������S�g����߂��铊����

�Ɛ������ǎ҂̃u�����b�Z���ł̋��c�ŁA�u����I�v�Ȑi�W�����������Ƃ𖾂炩�ɂ����B�h�h�e�̃_���[���ꖱ�����́u����I�����A�c�_��

�i�W���Ă���v�Ƃ̐����\�����B

59 �F���o�Â鏈�̖������F2011/10/23(��) 14:02:50.25 ID:ZLMKxJgC

ttp://mainichi.jp/select/biz/news/20111023k0000e020031000c.html

�s��F���j�I�~���A���������c���B��ӂ��œ_�@�@�����V���@2011�N10��23���@13��00��

�Q�P���̃j���[���[�N�O���ב֎s��ŁA�~���ꂪ�ꎞ�A�P�h�����V�T�~�V�W�K�܂ŏ㏸���A�W���P�X���̃j���[���[�N�s��ł������ō��l

�i�V�T�~�X�T�K�j���Q�J���Ԃ�ɍX�V�����B���B����@�Ȃǂ�w�i�ɔ�r�I���S�ȉ~�Ɏ������������₷�����������Ă���A���j�I�~��

�͒��������������B�s��̊S�́A���B��@�������߂̂��߂̕�I�ȑQ�U���̃��[������]��c�܂łɑł��o����邩�ɏW�܂��Ă���A

�T�����̎s��͐_�o���ȑ���W�J���\�z�����B�y�E�c�~�A��v�ۏA�ԊԐ��L�z

�Q�P���ɉ~���}�L�����̂́A�v�l�����̂悤�Ȓ��ړI�Ȃ��������͂Ȃ��A���@����C�ɔ����i�߂��̂��v���Ƃ݂���B�w�i�ɂ́A�ĘA�M��

�����x������i�e�q�a�j�������������lj��ɘa��R�e�i�p�d�R�j�ϑ��ɉ����A�u�^�C�^���̔�Q���\�z�ȏ�ɐ[���ŁA���{��Ƃ��O�Ȃ�

�C�O���Y�p���ĉ~�������茳�ɒu���v�Ȃǂ̌������������͗l���B

����̑���̌��ʂ��ɂ��Ďs��ł́u���j�I�ȉ~���͒���������v�Ƃ̌������������B��n�T�E�r�l�a�b�����،��V�j�A���בփX�g���e�W

�X�g�́u���B����@��w�i�ɁA���ۂȂǂ̋@�֓����Ƃ����{���̉^�p�����𑝂₷���j�������ȂǁA�~���ɂȂ�₷�����ꂪ�����v�Ǝw�E�B

��ꐶ���o�ό������̛���`����ȃG�R�m�~�X�g���u�Čo�ς̌������O�����܂�A�N���ɂ��e�q�a���lj��ɘa�ɓ��ݐ�\��������A�~����

�͂������v�Ƃ݂Ă���B

�T�����ȍ~�̑���́A�s�m���ȗv�f�������A���ʂ��ɂ����������B�Q�U���ɊJ����郆�[������]��c�ŁA���B��@�����Ɍ���������

���ӂł��邩�́A�\�f�������Ȃ�����B���ӂ��x���A�u���]������A����ɉ~�������i�ޓW�J�����蓾��v�i�����_��E�肻�ȋ�s�`�[

�t�E�}�[�P�b�g�E�X�g���e�W�X�g�j�Ƃ̌���������A�g�����\�z�����B

�����{�P�Ƒ�Ɍ��E

���Z�~�������͂Q�Q���A�u�s���߂��������ɂ͒f�ł���Ή����Ƃ�v�ƈב։���̉\������������Ȃ��瓊�@�I�ȓ����������������B

�������A���{�P�Ƃňב֑���̗����ς���͓̂���A���{�͑Ή��ɋꗶ���Ă���B

����ɂ��A���{�����z�Q���~�K�͂̉~����������t�c���肵���������ɉ~���ō��l���X�V�����B���Z�������͂Q�P���̉�Łu���̑�ʼn~

���ɑł������Ă�����Ƃ��㉟���������v�Ƌ����������A�s��̔����͋t�������B

������Ƃ̎����J��x�����A���Y�E�����{�݂̍������n�����������Ƃւ̕⏕���x�̊g�[�ȂǑΏǗÖ@�I�ȃ��j���[�������A�s��ł́u�~

���̔��{�I�ȉ����ɂ͂Ȃ���Ȃ��v�i�A�i���X�g�j�Ƃ̌��������������B���~���ŗA�o�����ɂ��炳���Y�ƊE����́A���{�E����ɓ��ݍ�

������߂鐺�����܂��Ă���B�T�����ȍ~�A�~��������ɐi�߂A���{�͂W���S���ȗ��̈ב։����T�錩�ʂ����B

�����A�i�C�̐�s�����O�����܂��Ă��鉢�Ăɔ�ׁA�����{��k�Ђ���̕������v�����ꂩ��{�i��������{�͔�r�I���S�ȓ�����ƌ��Ȃ���

�Ă���A���Ă��瓦�����������ɂ��~�����̓����͓��ʁA��݂����ɂȂ��B���ہA�W���̉������~���X���͑����Ă���B

���Ă��A�o�ɗL���Ȏ����̒ʉ݈���e�F���Ă��錻��ł́A�~�������Ɍ��������ۋ��������t���邱�Ƃ͓���A�u���{�Ɏc���ꂽ��͔��

�Ɍ����Ă���v�i���{�W�ҁj�̂����Ԃ��B

�s��F���j�I�~���A���������c���B��ӂ��œ_�@�@�����V���@2011�N10��23���@13��00��

�Q�P���̃j���[���[�N�O���ב֎s��ŁA�~���ꂪ�ꎞ�A�P�h�����V�T�~�V�W�K�܂ŏ㏸���A�W���P�X���̃j���[���[�N�s��ł������ō��l

�i�V�T�~�X�T�K�j���Q�J���Ԃ�ɍX�V�����B���B����@�Ȃǂ�w�i�ɔ�r�I���S�ȉ~�Ɏ������������₷�����������Ă���A���j�I�~��

�͒��������������B�s��̊S�́A���B��@�������߂̂��߂̕�I�ȑQ�U���̃��[������]��c�܂łɑł��o����邩�ɏW�܂��Ă���A

�T�����̎s��͐_�o���ȑ���W�J���\�z�����B�y�E�c�~�A��v�ۏA�ԊԐ��L�z

�Q�P���ɉ~���}�L�����̂́A�v�l�����̂悤�Ȓ��ړI�Ȃ��������͂Ȃ��A���@����C�ɔ����i�߂��̂��v���Ƃ݂���B�w�i�ɂ́A�ĘA�M��

�����x������i�e�q�a�j�������������lj��ɘa��R�e�i�p�d�R�j�ϑ��ɉ����A�u�^�C�^���̔�Q���\�z�ȏ�ɐ[���ŁA���{��Ƃ��O�Ȃ�

�C�O���Y�p���ĉ~�������茳�ɒu���v�Ȃǂ̌������������͗l���B

����̑���̌��ʂ��ɂ��Ďs��ł́u���j�I�ȉ~���͒���������v�Ƃ̌������������B��n�T�E�r�l�a�b�����،��V�j�A���בփX�g���e�W

�X�g�́u���B����@��w�i�ɁA���ۂȂǂ̋@�֓����Ƃ����{���̉^�p�����𑝂₷���j�������ȂǁA�~���ɂȂ�₷�����ꂪ�����v�Ǝw�E�B

��ꐶ���o�ό������̛���`����ȃG�R�m�~�X�g���u�Čo�ς̌������O�����܂�A�N���ɂ��e�q�a���lj��ɘa�ɓ��ݐ�\��������A�~����

�͂������v�Ƃ݂Ă���B

�T�����ȍ~�̑���́A�s�m���ȗv�f�������A���ʂ��ɂ����������B�Q�U���ɊJ����郆�[������]��c�ŁA���B��@�����Ɍ���������

���ӂł��邩�́A�\�f�������Ȃ�����B���ӂ��x���A�u���]������A����ɉ~�������i�ޓW�J�����蓾��v�i�����_��E�肻�ȋ�s�`�[

�t�E�}�[�P�b�g�E�X�g���e�W�X�g�j�Ƃ̌���������A�g�����\�z�����B

�����{�P�Ƒ�Ɍ��E

���Z�~�������͂Q�Q���A�u�s���߂��������ɂ͒f�ł���Ή����Ƃ�v�ƈב։���̉\������������Ȃ��瓊�@�I�ȓ����������������B

�������A���{�P�Ƃňב֑���̗����ς���͓̂���A���{�͑Ή��ɋꗶ���Ă���B

����ɂ��A���{�����z�Q���~�K�͂̉~����������t�c���肵���������ɉ~���ō��l���X�V�����B���Z�������͂Q�P���̉�Łu���̑�ʼn~

���ɑł������Ă�����Ƃ��㉟���������v�Ƌ����������A�s��̔����͋t�������B

������Ƃ̎����J��x�����A���Y�E�����{�݂̍������n�����������Ƃւ̕⏕���x�̊g�[�ȂǑΏǗÖ@�I�ȃ��j���[�������A�s��ł́u�~

���̔��{�I�ȉ����ɂ͂Ȃ���Ȃ��v�i�A�i���X�g�j�Ƃ̌��������������B���~���ŗA�o�����ɂ��炳���Y�ƊE����́A���{�E����ɓ��ݍ�

������߂鐺�����܂��Ă���B�T�����ȍ~�A�~��������ɐi�߂A���{�͂W���S���ȗ��̈ב։����T�錩�ʂ����B

�����A�i�C�̐�s�����O�����܂��Ă��鉢�Ăɔ�ׁA�����{��k�Ђ���̕������v�����ꂩ��{�i��������{�͔�r�I���S�ȓ�����ƌ��Ȃ���

�Ă���A���Ă��瓦�����������ɂ��~�����̓����͓��ʁA��݂����ɂȂ��B���ہA�W���̉������~���X���͑����Ă���B

���Ă��A�o�ɗL���Ȏ����̒ʉ݈���e�F���Ă��錻��ł́A�~�������Ɍ��������ۋ��������t���邱�Ƃ͓���A�u���{�Ɏc���ꂽ��͔��

�Ɍ����Ă���v�i���{�W�ҁj�̂����Ԃ��B

60 �F���o�Â鏈�̖������F2011/10/23(��) 14:11:46.04 ID:ZLMKxJgC

�����[������]��c�ŁA���B��@�����Ɍ��������ɍ��ӂł��邩�́A�\�f�������Ȃ�����B���ӂ��x���A�u���]������A�����

���~�������i�ޓW�J�����蓾��v�i�����_��E�肻�ȋ�s�`�[�t�E�}�[�P�b�g�E�X�g���e�W�X�g�j�Ƃ̌���������A�g�����\�z�����B

�������f�B�A�̓��[��������@���A���{�Ƃ͖��W�Ǝv���Ă��邩�̂悤�ŁA�܂Ƃ��ɕ��Ă��炸�A���͂����ȑO�Ɏ��Ԃ��������

�`����u�̐ӔC�v��������Ă���悤�Ɍ�����B������Ȃ������I�Ȑ���L��������ۂ��A���`�����v���p�K���_�̃S�~�L�����f�ڂ���

����ŁA�䂪���ɂ��בւ������ʂ��đ���̉e����^������j�I�Ȍo�ώ����ɖ��ڒ��ŁA����ʂĂ�B�@���B������̊�@�̎������@��

������A���������Ɍ������\����������WWII��̉��B�̐i��ł����R�[�X���ς��\����������̂ɁE�E�E�Ƃɂ������̍��ɂ�

�܂Ƃ��ȃW���[�i���Y�����ЂƂ����݂��Ȃ��B

���~�������i�ޓW�J�����蓾��v�i�����_��E�肻�ȋ�s�`�[�t�E�}�[�P�b�g�E�X�g���e�W�X�g�j�Ƃ̌���������A�g�����\�z�����B

�������f�B�A�̓��[��������@���A���{�Ƃ͖��W�Ǝv���Ă��邩�̂悤�ŁA�܂Ƃ��ɕ��Ă��炸�A���͂����ȑO�Ɏ��Ԃ��������

�`����u�̐ӔC�v��������Ă���悤�Ɍ�����B������Ȃ������I�Ȑ���L��������ۂ��A���`�����v���p�K���_�̃S�~�L�����f�ڂ���

����ŁA�䂪���ɂ��בւ������ʂ��đ���̉e����^������j�I�Ȍo�ώ����ɖ��ڒ��ŁA����ʂĂ�B�@���B������̊�@�̎������@��

������A���������Ɍ������\����������WWII��̉��B�̐i��ł����R�[�X���ς��\����������̂ɁE�E�E�Ƃɂ������̍��ɂ�

�܂Ƃ��ȃW���[�i���Y�����ЂƂ����݂��Ȃ��B

61 �F���o�Â鏈�̖������F2011/10/23(��) 14:34:17.90 ID:3tWUoKU3

�h���~����ɂ������̂Ƃ���͉�����ĂȂ���

�����͕��u�v���C�c

�����͕��u�v���C�c

62 �F���o�Â鏈�̖������F2011/10/23(��) 14:44:32.89 ID:VlH6/a1g

TPP���܂߂ăO���[�o���Y�����Ċ�Ƃɂ͂������Ƃ����邩������Ȃ����ǁA

�J���҂ɂƂ��Ă͂��܂肢�����Ƃł͂Ȃ���ˁc�B

��{�I�ɒ����������Ȃ邩��C�O�ɍs�����ǁA

�C�O�̒����̈����͘J���������������琬�藧���Ă�ʂ�����B

OHSAS��ISO�ɂȂ�Ȃ��̂������ƂɘJ�������ɍ������肷���邩��

���Ȃ�������������̂����R�������͂��B

�J���҂ɂƂ��Ă͂��܂肢�����Ƃł͂Ȃ���ˁc�B

��{�I�ɒ����������Ȃ邩��C�O�ɍs�����ǁA

�C�O�̒����̈����͘J���������������琬�藧���Ă�ʂ�����B

OHSAS��ISO�ɂȂ�Ȃ��̂������ƂɘJ�������ɍ������肷���邩��

���Ȃ�������������̂����R�������͂��B

63 �F���o�Â鏈�̖������F2011/10/23(��) 14:56:54.76 ID:JqxrkPQ6

>>57

���Ȏ��{�䗦�K���̋����͉������߂Ƃ��E�E�E�E

���Ȏ��{�䗦�K���̋����͉������߂Ƃ��E�E�E�E

64 �F���o�Â鏈�̖������F2011/10/23(��) 14:58:44.36 ID:ZLMKxJgC

ttp://www.forbes.com/sites/merrillmatthews/2011/10/21/the-red-state-in-your-future/

The Red State in Your Future�@10/21/2011 @ 12:40PM |47,221 views

���a�}�̎x�z����B�ƁA����}�̎x�z����B�̈Ⴂ�@�@�t�H�[�u�X�@�@21��

According to the National Conference of State Legislatures (NCSL), 25 state legislatures are controlled by Republicans and 16 by

Democrats, with eight split (i.e., each party controlling one house). There are 29 Republican governors and 20 Democrats, with one

independent. And there are 20 states where Republicans control both the legislature and governor�fs mansion vs. 11 Democratic, with

18 split (one party controls the governor�fs office and the other the legislature).

NCSL�̎����Ɉ˂�A�A�����J�̏��B�̂���29�̏B�͋��a�}�̏B�m�����A20�̏B�͖���}�̏B�m��������B��̏B�����}�h�̏B�m���ł���B

�B�c��̏㉺�@�����a�}�̗}����B��25�A����}�̎x�z����B��16�����āA8�̏B�ł͏㉺�@���ʂ̓}�Ɏx�z����Ă���B������܂Ƃ߂��

20�̏B�ŏB�m���Ƌc��㉺�@�����a�}���}���A����}��11�̏B��}���Ă���18�̏B�ł͒m���Ƌc���ʂ̐��}���}���Ă���B���̃f�[�^����

�B�����a�}���i���b�h�B�j���邢�͖���}���i�u���[�B�j�ɋ�ʂł���B

What�fs clear is that red or red-leaning states dominate the top positions while blue states have the dubious distinction of dragging

in last. In the economic outlook section, for example, the top 20 states are bright red or lean red, while eight out of the bottom

10 are very blue: New York, Vermont, California, Hawaii, New Jersey, Illinois, Oregon and Rhode Island.

�B�̍����o�Ϗ̌��ʂ����݂�ƃg�b�v20�̏B�̓��b�h�B�����̓��b�h�X�̏B�ŁA�Œ�ӂ�10�̏B�̂���8�̏B���Z���u���[�ł���B����

�̓j���[���[�N�A���@�[�����g�A�J���t�H���j�A�A�n���C�A�j���[�W���[�W�[�A�C���m�C�A�I���S���A���[�h�A�C�����h�ł���B

As commentator Michael Medved points out: �gBetween 2009 and 2010 the five biggest losers in terms of �eresidents lost to other states�f

were all prominent redoubts of progressivism: California, New York, Illinois, Michigan, and New Jersey. Meanwhile, the five biggest

winners in the relocation sweepstakes are all commonly identified as red states in which Republicans generally dominate local politics:

Florida, Texas, North Carolina, Arizona, and Georgia.�h

2009�N��2010�N�ŁA�B�ւ̐l�����������͗����Ō������A�Z���̗����̑傫����������v5�̏B�́A�J���t�H���j�A�A�j���[���[�N�A�C���m�C�A

�~�V�K���A�j���[�W���[�W�[�B�l�������̑��������g�b�v5�̏B�͂���������b�h�B�̃t�����_�A�e�L�T�X�A�m�[�X�J�����C�i�A�A���]�i�A�W���[�W�A

�ł������B

The Red State in Your Future�@10/21/2011 @ 12:40PM |47,221 views

���a�}�̎x�z����B�ƁA����}�̎x�z����B�̈Ⴂ�@�@�t�H�[�u�X�@�@21��

According to the National Conference of State Legislatures (NCSL), 25 state legislatures are controlled by Republicans and 16 by

Democrats, with eight split (i.e., each party controlling one house). There are 29 Republican governors and 20 Democrats, with one

independent. And there are 20 states where Republicans control both the legislature and governor�fs mansion vs. 11 Democratic, with

18 split (one party controls the governor�fs office and the other the legislature).

NCSL�̎����Ɉ˂�A�A�����J�̏��B�̂���29�̏B�͋��a�}�̏B�m�����A20�̏B�͖���}�̏B�m��������B��̏B�����}�h�̏B�m���ł���B

�B�c��̏㉺�@�����a�}�̗}����B��25�A����}�̎x�z����B��16�����āA8�̏B�ł͏㉺�@���ʂ̓}�Ɏx�z����Ă���B������܂Ƃ߂��

20�̏B�ŏB�m���Ƌc��㉺�@�����a�}���}���A����}��11�̏B��}���Ă���18�̏B�ł͒m���Ƌc���ʂ̐��}���}���Ă���B���̃f�[�^����

�B�����a�}���i���b�h�B�j���邢�͖���}���i�u���[�B�j�ɋ�ʂł���B

What�fs clear is that red or red-leaning states dominate the top positions while blue states have the dubious distinction of dragging

in last. In the economic outlook section, for example, the top 20 states are bright red or lean red, while eight out of the bottom

10 are very blue: New York, Vermont, California, Hawaii, New Jersey, Illinois, Oregon and Rhode Island.

�B�̍����o�Ϗ̌��ʂ����݂�ƃg�b�v20�̏B�̓��b�h�B�����̓��b�h�X�̏B�ŁA�Œ�ӂ�10�̏B�̂���8�̏B���Z���u���[�ł���B����

�̓j���[���[�N�A���@�[�����g�A�J���t�H���j�A�A�n���C�A�j���[�W���[�W�[�A�C���m�C�A�I���S���A���[�h�A�C�����h�ł���B

As commentator Michael Medved points out: �gBetween 2009 and 2010 the five biggest losers in terms of �eresidents lost to other states�f

were all prominent redoubts of progressivism: California, New York, Illinois, Michigan, and New Jersey. Meanwhile, the five biggest

winners in the relocation sweepstakes are all commonly identified as red states in which Republicans generally dominate local politics:

Florida, Texas, North Carolina, Arizona, and Georgia.�h

2009�N��2010�N�ŁA�B�ւ̐l�����������͗����Ō������A�Z���̗����̑傫����������v5�̏B�́A�J���t�H���j�A�A�j���[���[�N�A�C���m�C�A

�~�V�K���A�j���[�W���[�W�[�B�l�������̑��������g�b�v5�̏B�͂���������b�h�B�̃t�����_�A�e�L�T�X�A�m�[�X�J�����C�i�A�A���]�i�A�W���[�W�A

�ł������B

65 �F���o�Â鏈�̖������F2011/10/23(��) 15:00:06.99 ID:ZLMKxJgC

By contrast, some blue states appear determined to spend themselves into bankruptcy. The AP reported on Oct. 16, �gDrowning in

deficits, Illinois has turned to a deliberate policy of not paying billions of dollars in bills for months at a time.�c�h So that big

tax increase passed by Obama�fs home state, which likes to do things the Obama way, didn�ft fix the revenue problem. Someone needs to

call the president and explain that to him.

���b�h�B����ʂɍ����ێ�h�Ō��łɑO�����ł���̂ɔ�ׂău���[�B�͕��������Ŕj�Y�Ɍ������悤�Ȍ����x�o�������B10��16���ɂ�AP�̋L��

���C���m�C�B�̍����̈����ɂ�葝�łɓ��ݐ�ƕĂ���B

Many fed-up citizens in those blue states are leaving. But others have decided that if anyone is going to leave, it�fs those

big-spending politicians who brought on the fiscal disaster. It�fs a lesson blue-state politicians better learn: It�fs better to be

red than dead.

�u���[�B�̏Z�����A���̏B���̂Ăă��b�h�B�Ɉڂ�Z�ތX���Ƃ����̂́A���������B���{�̍����K���̂Ȃ��Ƒ��Ő���Ɍ���������B�i�㗪�j

deficits, Illinois has turned to a deliberate policy of not paying billions of dollars in bills for months at a time.�c�h So that big

tax increase passed by Obama�fs home state, which likes to do things the Obama way, didn�ft fix the revenue problem. Someone needs to

call the president and explain that to him.

���b�h�B����ʂɍ����ێ�h�Ō��łɑO�����ł���̂ɔ�ׂău���[�B�͕��������Ŕj�Y�Ɍ������悤�Ȍ����x�o�������B10��16���ɂ�AP�̋L��

���C���m�C�B�̍����̈����ɂ�葝�łɓ��ݐ�ƕĂ���B

Many fed-up citizens in those blue states are leaving. But others have decided that if anyone is going to leave, it�fs those

big-spending politicians who brought on the fiscal disaster. It�fs a lesson blue-state politicians better learn: It�fs better to be

red than dead.

�u���[�B�̏Z�����A���̏B���̂Ăă��b�h�B�Ɉڂ�Z�ތX���Ƃ����̂́A���������B���{�̍����K���̂Ȃ��Ƒ��Ő���Ɍ���������B�i�㗪�j

66 �F���o�Â鏈�̖������F2011/10/23(��) 15:08:09.39 ID:BPtbio5e

�����������@�r�㍑�u�m�n�v�@�~�����}�[�A�_���J�����~��\���i2011/10/04-07:56�j

ttp://sankei.jp.msn.com/world/news/111004/chn11100407580006-n1.htm

��

���y�~�����}�[�z�~�����}�[������_�����z���f�̕��j�\�u�����ł��Ȃ��v�Ƌ������z�̒�����Ɣ���[10/07]

�@�@http://kamome.2ch.net/test/read.cgi/news4plus/1317982929/

��

��

�����l�D���E�Q�@���܂�ْ��i2011/10/05�j

ttp://sankei.jp.msn.com/world/news/111016/chn11101612010002-n1.htm

�^�C�����̃��R���쐅���10��5���A�����l��g�����悹�����D�Q�ǂ��������͂̏P������12�l���E�Q

���܂�����A�����R���������ی�̖��ڂŁA�C�O�h�����ă��R���쉈�݂��x�����邱�Ƃ����߂�ӌ�(by�R�W��)

�@�@�@�@�@�@�@�@~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

�@�����̕����l�B�́A���͒������Y�}�ɒǂ�ꂽ�������{�R�̎c�}�i�����l�j�Ƃ̂���

�@�@�@���������̏�́A�^�A�E�o�ςƂ��ɏd�v�Ȓn��

India offers Myanmar $500m Line of Credit�i2011/10/15�j

ttp://indiatoday.intoday.in/story/india-offers-myanmar-$500m-line-of-credit/1/155050.html

�C���h���{�̓~�����}�[�̃e�C���Z�C���哝�̂d�Ɍ}���A5���h����LOC��ݒ�B

�K���3���h���ɏ�悹������̂ŁA�C���t���i���H�E���d���E���j�h�s�ȂǑΏۂƂ���Ƃ̔��\�B

��

��

�@India welcomes China's decision not to divert Bhrahmaputra�i2011/10/14�j

�@ttp://www.indianexpress.com/news/india-welcomes-chinas-decision-not-to-divert-bhrahmaputra/859965/

�@�C���h�̃N���V���i�O����b�́A�������u���}�v�g���͂̕�������߂����ƂɊ��}�̈ӁB

�@���̒k�b�́A�~�����}�[�哝�̂Ƃ̉�k�̒���ɂȂ��ꂽ�Ƃ̂��ƁB

�@��

�@���y�Q�l�z�C���h�ƒ����Ƃ̊Ԃɐ����߂��镴���̖G��i2011/10/20�j

�@�@�C���h�ɗ��ꍞ�މ͐���A�������㗬�ŕ���

�@ttp://business.nikkeibp.co.jp/article/world/20110914/222646/

ttp://sankei.jp.msn.com/world/news/111004/chn11100407580006-n1.htm

��

���y�~�����}�[�z�~�����}�[������_�����z���f�̕��j�\�u�����ł��Ȃ��v�Ƌ������z�̒�����Ɣ���[10/07]

�@�@http://kamome.2ch.net/test/read.cgi/news4plus/1317982929/

��

��

�����l�D���E�Q�@���܂�ْ��i2011/10/05�j

ttp://sankei.jp.msn.com/world/news/111016/chn11101612010002-n1.htm

�^�C�����̃��R���쐅���10��5���A�����l��g�����悹�����D�Q�ǂ��������͂̏P������12�l���E�Q

���܂�����A�����R���������ی�̖��ڂŁA�C�O�h�����ă��R���쉈�݂��x�����邱�Ƃ����߂�ӌ�(by�R�W��)

�@�@�@�@�@�@�@�@~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

�@�����̕����l�B�́A���͒������Y�}�ɒǂ�ꂽ�������{�R�̎c�}�i�����l�j�Ƃ̂���

�@�@�@���������̏�́A�^�A�E�o�ςƂ��ɏd�v�Ȓn��

India offers Myanmar $500m Line of Credit�i2011/10/15�j

ttp://indiatoday.intoday.in/story/india-offers-myanmar-$500m-line-of-credit/1/155050.html

�C���h���{�̓~�����}�[�̃e�C���Z�C���哝�̂d�Ɍ}���A5���h����LOC��ݒ�B

�K���3���h���ɏ�悹������̂ŁA�C���t���i���H�E���d���E���j�h�s�ȂǑΏۂƂ���Ƃ̔��\�B

��

��

�@India welcomes China's decision not to divert Bhrahmaputra�i2011/10/14�j

�@ttp://www.indianexpress.com/news/india-welcomes-chinas-decision-not-to-divert-bhrahmaputra/859965/

�@�C���h�̃N���V���i�O����b�́A�������u���}�v�g���͂̕�������߂����ƂɊ��}�̈ӁB

�@���̒k�b�́A�~�����}�[�哝�̂Ƃ̉�k�̒���ɂȂ��ꂽ�Ƃ̂��ƁB

�@��

�@���y�Q�l�z�C���h�ƒ����Ƃ̊Ԃɐ����߂��镴���̖G��i2011/10/20�j

�@�@�C���h�ɗ��ꍞ�މ͐���A�������㗬�ŕ���

�@ttp://business.nikkeibp.co.jp/article/world/20110914/222646/

67 �F���o�Â鏈�̖������F2011/10/23(��) 15:09:26.13 ID:FtbzGwMV

�y�����z �s�o�o�Q���h�E�É����̐쏟�m���u���i�ƕi��������̂ŁA�����ɑ���Ȃ��v�@���{���i��_�Y���̗D�ʐ��������@�@

ttp://raicho.2ch.net/test/read.cgi/newsplus/1319349638/

�d�g���Ȃɂ������Ă��d�g����ȁ`

ttp://raicho.2ch.net/test/read.cgi/newsplus/1319349638/

�d�g���Ȃɂ������Ă��d�g����ȁ`

68 �F���o�Â鏈�̖������F2011/10/23(��) 15:50:48.28 ID:jG372XEn

�����ŐӔC�����Ȃ����Ƃ����₷���y���y��������Ȃ�

69 �F���o�Â鏈�̖������F2011/10/23(��) 16:05:41.24 ID:8sM/rS/e

70 �F���o�Â鏈�̖������F2011/10/23(��) 16:16:06.98 ID:RhQ9AU1j

>>67

����ς�É��Ő��E�I�ɋ����͂̂���_�앨�݂͂���Ƃ������H

����Ȃ̂ŊO����������Ă���i���_�앨�Ə����o����Ǝv���Ă�̂��H

����ς�É��Ő��E�I�ɋ����͂̂���_�앨�݂͂���Ƃ������H

����Ȃ̂ŊO����������Ă���i���_�앨�Ə����o����Ǝv���Ă�̂��H

71 �F���o�Â鏈�̖������F2011/10/23(��) 16:19:42.73 ID:jG372XEn

�C�O��������Ă���̂́A�h�[����f�������e��R�J�R�[���{�g���[�Y�B

�_���͔_�z�ƂȂ��ă~�J���₨��������āA�i���Ŕ����āA

�X�e�L�ȓ��{���W���[�X�������ʂ̏o���オ��B

�_���͔_�z�ƂȂ��ă~�J���₨��������āA�i���Ŕ����āA

�X�e�L�ȓ��{���W���[�X�������ʂ̏o���オ��B

72 �F���o�Â鏈�̖������F2011/10/23(��) 16:25:45.74 ID:G7THbgze

>>70

���{�̒��t�͂����ł����_��吙�ʼn��B�ɏo�����ɂ����̂�

����̑����œ����A�o�͖�������ˁH

���Ƃ����˔\����܂���Əؖ���

�Y�t���Ă����߁B�C���̖�肾���ˁB

���{�̒��t�͂����ł����_��吙�ʼn��B�ɏo�����ɂ����̂�

����̑����œ����A�o�͖�������ˁH